I spent last night clicking through every single tenure option inside my Shopee Loan Simulation screen. ₱100,000 at 3 months. At 6 months. At 9. At 12. I took a screenshot of each one, because I want to show you the real figures before you click that Activate Now button.

Here's what I found. A ₱100,000 loan over 12 months costs ₱13,283.33 per month based on what Shopee quoted my account, which adds up to ₱159,400 total and ₱59,400 in interest.

The same ₱100,000 loan over 3 months costs ₱38,283.33 per month, but only ₱14,850 in total interest. Same loan, same 4.95% monthly installment fee rate as quoted to my account, four times the interest for choosing the longer term.

Nobody shows you that math. Most articles quote Shopee's official range of "1% to 5% monthly" and leave you to figure out what it means for your wallet.

This guide is different. Every number here comes either from my own Shopee app screen or from Shopee's official Help Center, cited directly. If you're thinking about activating SLoan, read this first. ? A quick note before we dive in.This article is general financial information, not personalized financial advice. The rates, fees, and repayment figures shown are accurate as of May 2026, based on my own Shopee Loan Simulation screens and Shopee's official Help Center. Your actual rate, credit limit, and approval status may differ from mine. Total loan cost includes interest, processing fees, and other charges as applicable.Before you activate any loan product, please verify the current terms directly inside your Shopee app and consider consulting a licensed financial advisor if you're unsure whether borrowing is the right move for your situation. Always verify rates with the official source before signing up: Shopee PH Help Center.

Jump to a section

- What is Shopee Loan (SLoan)?

- SLoan vs SPayLater: which one are you actually using?

- Who can apply for Shopee Loan?

- How to activate Shopee Loan step by step

- Shopee Loan interest rates and the real cost of borrowing

- Shopee Loan calculator: every tenure, side by side

- How to withdraw Shopee Loan to GCash or your bank

- How to pay your Shopee Loan bill

- What happens if you don't pay: penalties, frozen accounts, and legal truth

- How to increase your Shopee Loan credit limit

- Is Shopee Loan worth it? My honest take

- Where to verify: official sources

What is Shopee Loan (SLoan)?

SLoan is a cash loan product offered through the Shopee app. Shopee's Help Center describes it as a fast way to get cash loans with "competitive interest rates and flexible repayment terms of 1, 3, 6, 9, or 12 months."

Once your loan is approved, the cash is credited to your ShopeePay wallet, where you can use it to buy items, send money, or withdraw to a bank account. You can borrow anywhere from ₱2,500 to ₱100,000, depending on your assigned credit limit.

The financing company behind SLoan is SeaMoney (Credit) Finance Philippines Inc., part of the same Sea Group that operates Shopee.

Before you borrow, verify SeaMoney's current registration status directly on the Philippine Securities and Exchange Commission website. Registration does not equal endorsement or consumer protection guarantee. But it is the baseline legitimacy check for any financing or lending company operating in the Philippines.

SLoan vs SPayLater: which one are you actually using?

These two products get confused constantly, and that confusion costs people money. SPayLater is a buy-now-pay-later feature.

It lets you check out items on Shopee and pay for them in installments, with interest rates of 1% to 5% per month on the total order and a processing fee of 0% to 7%, per Shopee's published range as of May 2026.

SLoan is a straight-up cash loan. The money lands in your ShopeePay wallet and you can do whatever you want with it: transfer to GCash, pay bills, withdraw to your bank.

The simplest way to tell them apart: SPayLater buys things. SLoan gives you cash. They also have separate credit limits and separate late payment consequences. An overdue SPayLater balance can get your SLoan account frozen, and vice versa.

Who can apply for Shopee Loan?

According to Shopee's official activation page, eligible users must be Filipino, aged 21 to 65 years old, and have a good credit score based on Shopee's internal assessment.

There's no public application form. SLoan is invitation-based. If you see the SLoan option inside your Shopee app under the Finance page or Me tab, you're eligible. If you don't see it, Shopee hasn't extended an offer to your account yet.

Based on my personal experience, since I consistently pay my SPayLater, I have observed that the more Shopee increases my credit limit, the more it opens the door for SLoan on my account.

Shopee doesn't publicly disclose the exact factors that go into their credit assessment.

Based on Shopee's own published materials, a clean payment history on SPayLater, active ShopeePay wallet usage, and consistent Shopee activity are reasonable signals to maintain. If your account is brand new or rarely used, expect to wait.

How to activate Shopee Loan step by step

Shopee's Help Center lays out a straightforward activation flow.

- First, go to the Finance page or tap your Me tab, then select SLoan.

- Tap Activate Now. Enter the One-Time Password (OTP) sent to your registered number.

- Upload a valid government-issued ID. Shopee accepts Philippine Passport, Driver's License, UMID, Postal ID, PRC ID, TIN ID for selected users, PhilSys ID, SSS, Phil ID, PhilHealth ID, ePhil ID, and Digital National ID.

- Complete the liveness check. You'll get a notification of your approval within 24 hours.

If your app doesn't show the Activate Now button, the product isn't available to you yet.

Shopee customer service cannot manually activate it on request. The offer has to surface organically in your app based on their credit criteria.

Shopee Loan interest rates and the real cost of borrowing

Here's where most articles get vague and where this guide gets specific.

According to Shopee's official SLoan fees page, as of May 2026, the monthly interest rate ranges from 1% to 5% of the total loan principal, and the rate you actually get "may differ from the rates offered to other borrowers" depending on Shopee's internal credit assessment.

There's also an admin fee of 0% to 2% of the principal, deducted upfront from your disbursement, and an optional Loan Protection fee of 0.2% per month.

What does this look like in real pesos?

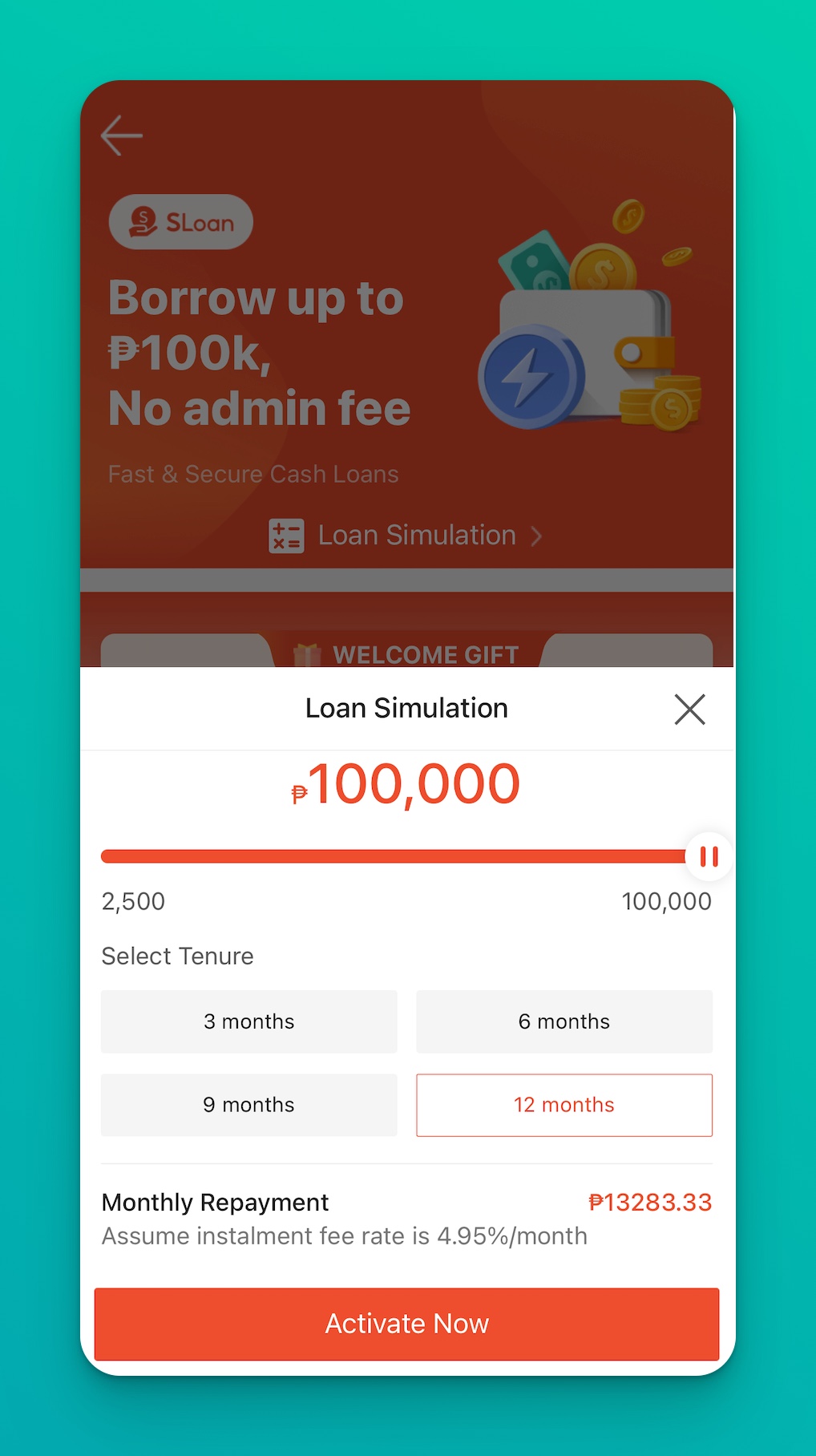

My Shopee Loan Simulation screen quoted me 4.95% per month for every tenure I tested, with no admin fee and a welcome gift of 15% off the interest rate, valid until May 31, 2026.

On a ₱100,000 loan at 12 months, the monthly repayment was ₱13,283.33. That's for my account as of May 2026. Your rate may differ.

Multiply ₱13,283.33 by 12 and you get ₱159,400. That's ₱59,400 in interest on a ₱100,000 loan over one year.

When you annualize the quoted flat monthly rate using the standard add-on structure, the rough annualized borrowing cost approximation lands far higher than 4.95% x 12 suggests.

That's because the flat monthly rate is charged on the original principal every single month, even as your outstanding balance goes down. The point is not the exact annualized figure.

The point is that a quoted 4.95% monthly rate is meaningfully more expensive than many Filipino borrowers assume at first glance.

For context, as of May 2026, credit card interest in the Philippines is capped by the Bangko Sentral ng Pilipinas at around 36% per year based on its current ceiling circular.

A typical bank personal loan in the Philippines runs roughly 12% to 25% effective based on publicly published rates. SLoan, at the rate quoted to my account, can cost materially more than either of those options under those comparisons. Know the numbers before you tap Activate Now.

Shopee Loan calculator: every tenure, side by side

Shopee has a built-in Loan Simulation tool inside the app. Open SLoan, tap Loan Simulation, slide to your preferred amount, and pick a tenure of 3, 6, 9, or 12 months. The app will show you the monthly repayment at your personalized installment fee rate.

Here's what Shopee actually quoted my account across every tenure on a ₱100,000 loan, all at the same 4.95% monthly installment fee rate.

These are direct screenshots from my own Shopee Loan Simulation as of May 2026, not estimates, and your actual rate and fees may vary based on Shopee's internal credit assessment:

Tenure | Monthly Repayment | Total Payable | Total Interest | Interest as % of Principal |

|---|---|---|---|---|

3 months | ₱38,283.33 | ₱114,850.00 | ₱14,850.00 | 14.85% |

6 months | ₱21,616.67 | ₱129,700.00 | ₱29,700.00 | 29.70% |

9 months | ₱16,061.11 | ₱144,550.00 | ₱44,550.00 | 44.55% |

12 months | ₱13,283.33 | ₱159,400.00 | ₱59,400.00 | 59.40% |

Shopee Loan repayment schedule: ₱100,000 at 4.95% monthly, as quoted to the author's account. Source: author's Shopee app Loan Simulation, May 2026. Your actual rate and fees may vary. Look at the interest column. The 12-month tenure costs ₱59,400 in interest. The 3-month tenure costs ₱14,850. Same loan amount, same monthly rate, four times the interest for choosing the longer term.

A longer tenure looks kinder on your monthly cash flow, but at this rate, it quadruples what you actually pay back.

Smaller loans follow the same pattern. At the same quoted rate, a ₱10,000 loan over 3 months comes out to ₱3,828.33 per month, ₱11,485 total, ₱1,485 in interest, per my Loan Simulation screen. If you can pay it off in three months, do it.

Your personal rate may be lower.

Shopee's published range starts at 1% monthly for the best-qualified borrowers, which would drop all these numbers significantly. But don't assume. Open your app, run your own simulation across all four tenures, and screenshot what you see before you commit.

How to withdraw Shopee Loan to GCash or your bank

Once your SLoan is activated and approved, you request a withdrawal inside the app. The cash is credited to your ShopeePay wallet first.

From ShopeePay, you can transfer it to your linked bank account.

GCash transfers go through the same InstaPay or PESONet rails as any ShopeePay-to-bank transfer, and standard ShopeePay transfer fees apply.

If you try to withdraw and get blocked, Shopee's Help Center lists the usual reasons: an outstanding overdue balance on another credit facility like SPayLater, or a remaining credit limit below the minimum loan amount.

Settle the overdue amount first, and withdrawal access returns.

How to pay your Shopee Loan bill

Your SLoan monthly bill is deducted or paid inside the Shopee app. Shopee is firm about this: "Only pay your bills inside the Shopee app, never through links or platforms outside Shopee." If someone messages you a payment link for your Shopee Loan, it's a scam.

Inside the app:

- Go to Me tab, then SLoan, then view your outstanding bill and pay from ShopeePay, a linked bank account, or your other supported payment channels.

- Set a monthly reminder on your phone for three days before the due date.

- Auto-debit from ShopeePay only works if your wallet has enough balance on the billing date.

What happens if you don't pay: penalties, frozen accounts, and legal truth

This is the section Filipinos search the most. "May nakukulong ba sa Shopee Loan" is one of the most searched Shopee Loan queries on Google, and the fear deserves a direct answer.

First, the Shopee consequences. According to Shopee's official repayment article, as of May 2026, a monthly late charge of 5% is added to the overdue amount if you miss your bill.

Your SLoan account can also be frozen, which means you cannot withdraw new loans, and your SPayLater account may be restricted as well.

To reactivate a frozen account, you have to settle the full overdue balance, after which the account is reactivated within 24 to 48 hours per Shopee's stated timeline.

Now the legal context.

In the Philippines, ordinary unpaid consumer debt is generally treated as a civil matter. Article III, Section 20 of the 1987 Philippine Constitution states that no person shall be imprisoned for debt. This section is not legal advice.

For guidance specific to your situation, consult a licensed Philippine lawyer.

In practical terms, a lender can still pursue collection, report the unpaid debt to credit bureaus, and file a civil case to recover what's owed. A court in a civil case can order repayment plus interest and penalties and enforce that judgment against assets, within the limits of Philippine law.

Defaulting still carries real consequences: damaged credit history, frozen Shopee accounts, and collection calls. Communicate with Shopee early if you're struggling. It's always better than hiding.

How to increase your Shopee Loan credit limit

Shopee does not publicly disclose a formal credit limit increase request form or a published formula for limit adjustments.

The limit is determined and adjusted by Shopee's internal credit assessment. What Shopee's own materials do make clear is that on-time repayment of SLoan and SPayLater bills, active ShopeePay wallet usage, and consistent account activity are the baseline behaviors the platform monitors.

Missed or late payments work the opposite direction. They can freeze your account and restrict your access to other Shopee credit products.

If you want a higher loan amount and Shopee isn't raising your limit, a traditional bank personal loan may serve you better.

Bank rates are typically lower than SLoan's quoted rate range based on publicly published rates as of May 2026, and approved amounts are typically higher for salaried borrowers with good credit history.

Is Shopee Loan worth it? My honest take

SLoan is fast. It's convenient. It lives inside an app you already use. For a small, short-term need, like a sudden ₱5,000 shortfall before payday or a ₱10,000 emergency you can clear in three months, it can solve a real problem, especially if Shopee gave you a lower personalized rate.

But at the rate quoted to my account, which is 4.95% per month, Shopee Loan can be one of the more expensive ways to borrow in the Philippines as of May 2026. Based on publicly published rates, it can cost materially more than a typical credit card cash advance, a typical bank personal loan, and a Pag-IBIG multi-purpose loan, which caps at around 10.75% per year and is available to active Pag-IBIG members.

Before you activate, ask yourself three questions.

- Can you pay this in three months or less? The calculator table above shows why that matters. At the rate quoted to my account, three months costs ₱14,850 in interest, twelve months costs ₱59,400.

- Do you actually need the cash, or is this a want? Emergency funds exist for a reason, and this is why Moneysmart keeps reminding readers to build a one-month buffer first.

- And is there a cheaper option? Check your credit card's cash advance rate, your company's salary loan, or a Pag-IBIG short-term loan before you tap Activate Now.

If you've weighed all that and SLoan still makes sense for your situation, go in with eyes open.

Read the simulation screen carefully. Note your actual monthly rate, because it may or may not match the 4.95% I was quoted. Pick the shortest tenure you can realistically afford. Set payment reminders. Never miss a due date. And pay it off as fast as you can.

Shopee Loan isn't evil. It's a financial product with a clear price tag, and the price tag is higher than most people realize before they tap Activate Now.

Now you know the actual numbers, the actual rules, and the actual consequences. What you do with that is up to you.

Have you used Shopee Loan before? What rate did Shopee quote you, and which tenure did you pick? Drop a comment below and let's compare notes.

Disclaimer: This article is published for general informational and educational purposes only. It does not constitute personalized financial, legal, or tax advice. Interest rates, fees, promos, and eligibility criteria cited are accurate as of May 2026 based on Shopee's official Help Center and the author's Shopee Loan Simulation screens. Actual rates, credit limits, and approval outcomes vary per borrower based on Shopee's internal credit assessment. Total loan cost includes interest, processing fees, and other charges as applicable. Please verify current terms directly with Shopee and consult a licensed financial advisor before making any borrowing decision.