The Home Development Mutual Fund, also referred to as PAG-IBIG, is often associated with affordable housing loans. But did you know active members also have access to other benefits beyond financing?

PAG-IBIG has three types of programs: savings, loans, and insurance. Fortunately, you don’t have to go to a PAG-IBIG branch to access these services. You can simply register through virtual PAG-IBIG.

In this article, you’ll learn how to quickly register for an account, what available programs are offered, and which benefits you can enjoy as an active member.

What is Virtual PAG-IBIG?

Virtual PAG-IBIG gives you 24/7 access to its services, such as membership registration, loan applications, online payments for contributions, and MP2 savings program.

Because it’s virtual, you don’t need to queue or join the crowds at the branch. You can access your account conveniently from the comfort of your own home.

What are the Virtual PAG-IBIG services you can access?

If you are formally employed, your PAG-IBIG remittances are handled by your employer. Your PAG-IBIG is one of your government-mandated benefits, like SSS and PhilHealth.

For self-employed individuals and OFWs, you need to register for your own PAG-IBIG account and make voluntary contributions to enjoy the perks.

Regular Savings Program

This where your monthly PAG-IBIG contribution goes. It’s an easy way to save and earn higher dividends. What’s more, it’s government-guaranteed.

You only need to put P100 every month for your PAG-IBIG savings. But you can always add more by requesting an upgrade to earn more dividends.

What’s great about this savings program is that dividend earnings are tax-free.

MP2 Savings Program

You may also voluntarily avail of the MP2 Savings Program. This is the Modified PAG-IBIG savings program that lets you earn higher dividends in addition to your regular savings.

The monthly base rate for contributions is P500, with dividend earnings up 7.00% per annum and a five-year maturity period. You can receive your dividend earnings annually or after five years.

Housing loans program

As a member, you get low-interest rates for housing loans starting from 4.985% per annum (as of this writing until 29 December 2020), subject to repricing after a year.

Qualified members with at least 24 months of savings can avail of a maximum loan amount of P6 million and apply with up to two co-borrowers.

The affordable housing program is open for minimum wage earners. They can apply for a housing loan of up to P450,000 with an interest rate of 3% per annum, or up to P750,000 with an interest rate of 6.5% per annum. Moreover, loan repayment periods can be up to 30 years, the longest tenure in the market.

Home insurance services

Last but not least, borrowers can avail of the Mortgage Redemption Insurance (MRI) that will cover the mortgage amortization if the principal borrower dies or is diagnosed with a terminal illness.

Other insurance services you can get also include fire and allied perils insurance. These are subject to properties taken from the housing loans, covering fire, earthquake, flood, and other natural disasters and accidents.

Other benefits of active PAG-IBIG members

As long as you have an active regular savings account, you enjoy other benefits such as the Multi-Purpose Loan (MPL). This is a cash loan for active members who need financial aid immediately.

You can borrow up to 80% of your total accumulated savings, and PAG-IBIG can process your application within two days.

PAG-IBIG also has a financial assistance program for members in calamity-stricken areas. The Calamity Loan Program allows members to borrow at a 5.95% per annum rate. It’s also one of the lowest market rates, payable in 24 months with a deferred first payment.

PAG-IBIG members can also get their Loyalty Card Plus to enjoy discounts and rewards. Use the card in PAG-IBIG’s partner merchants and participating establishments and get anywhere between 5% to 80% discount.

How to register on Virtual PAG-IBIG

If you want to become a member, visit the official Virtual PAG-IBIG website and click > Be a Member.

Fill out the form and click Next until you finish all the tabs. Upon completion, you will see a registration confirmation page. You will also receive an SMS notification that includes your tracking number.

Use the tracking number temporarily when remitting your contributions while you wait for your official PAG-IBIG membership number.

How to fund your PAG-IBIG account

Aside from remitting over the counter, you can also use cashless and contactless transactions through mobile banking or e-wallets. Here are a few convenient ways to do it.

Via GCash, CoinsPH and other e-wallets

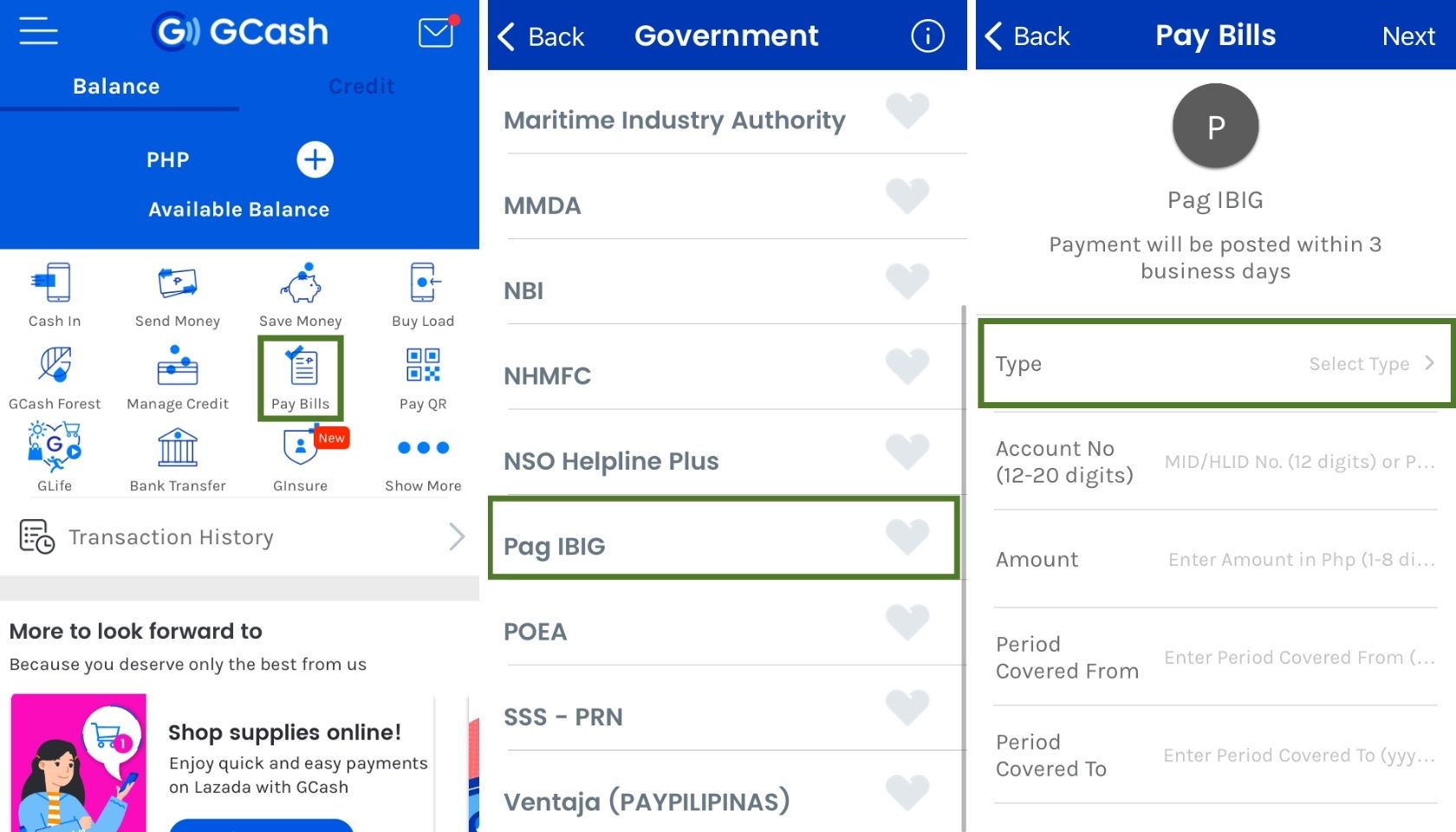

For GCash, follow the steps below.

- Open the GCash app and tap Pay Bills > Government > PAG-IBIG

- Tap ‘Type’ and choose the type of service you wish to fund: Members Contribution, Modified PAG-IBIG II Savings, or Housing Loan

- Then fill out the rest of the form with the account number, amount, and period covered.

- Click Next to finalize the payment and tap Confirm

With this method, your funds will reflect on your account within three business days. GCash also charges a P5 convenience fee per transaction.

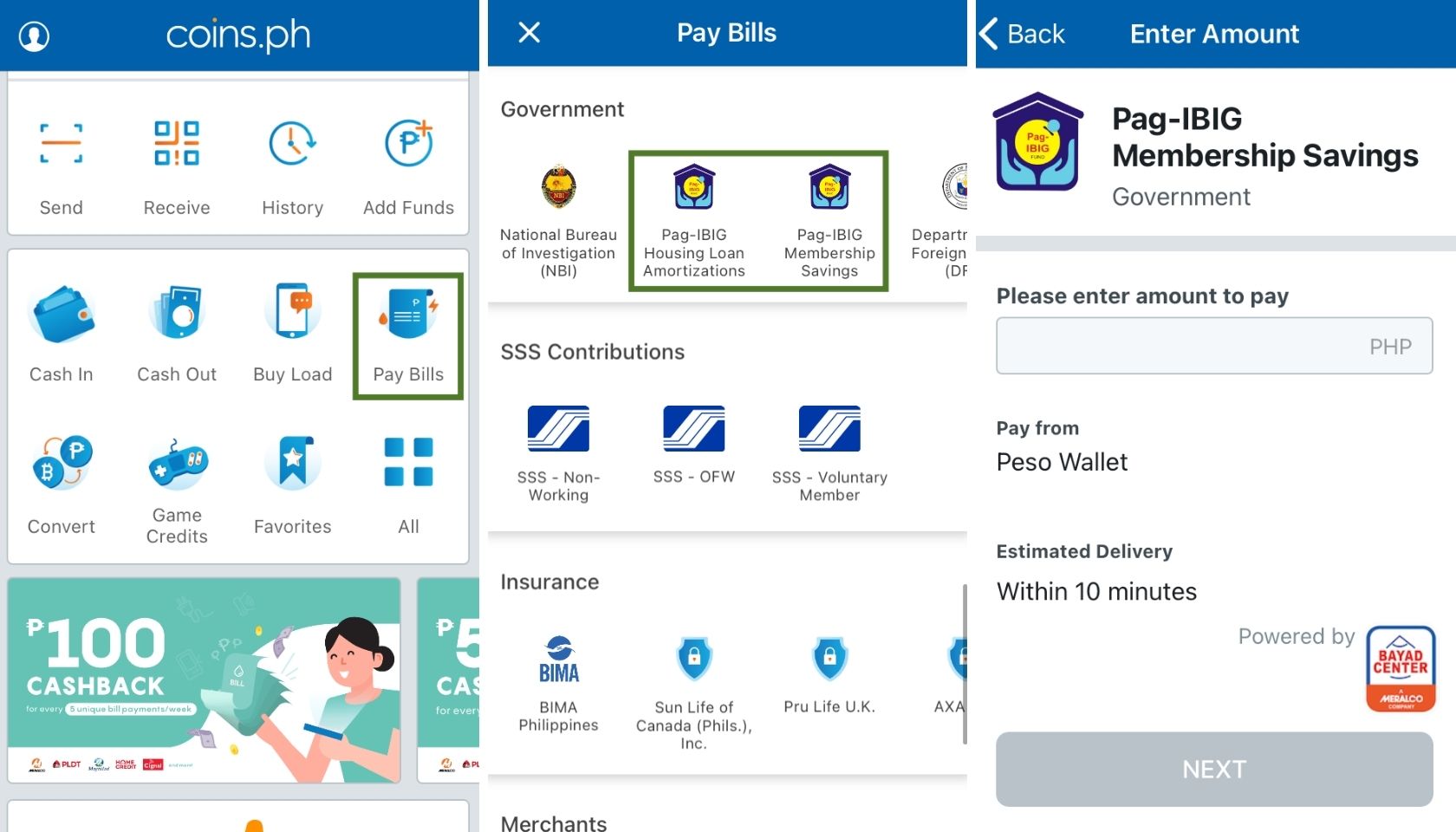

For CoinsPH, here’s how to fund your account.

- Launch your CoinsPH app, tap Pay Bills, scroll down to the Government section, and select either PAG-IBIG Housing Loan Amortization or PAG-IBIG Membership Savings.

- Enter the amount and click Next to enter details and to confirm your payment.

The convenience fee is P7, and the funds have an estimated delivery of 10 minutes. Payments made after the 8:00 PM cut-off are credited the following business day.

PayMaya also allows you to pay via its mobile app, but it will direct you to the official Virtual PAG-IBIG website, unlike GCash and CoinsPH wherein you can pay in-app.

You can also pay for your contributions via credit card, ECPay, and overseas remittance for Filipinos working abroad. Visit the payment portal for more info.

Final Thoughts — Should You Get One?

If you already have a PAG-IBIG account when you got employed, good for you! As long as you are employed, your contributions will be regularly updated.

You can also take advantage of the Modified PAG-IBIG 2 Savings program if you want to save more and want higher dividend earnings.

If you’re self-employed or a business owner, you can also pay your contributions in a lump sum of 24 months for quick access to other loan services.

So what’s not to love about PAG-IBIG if you can save and invest for as low as P100 or P500? Instead of spending your money on unnecessary luxuries, save and invest in your future.

Let us know which PAG-IBIG program we discussed above will serve you best at this stage of your life. Start a conversation in the comments below.