Ever heard of BNPL? If you ever shop online, you must have encountered it. It's an acronym for Buy Now, Pay Later, an agreement where a store lets you buy now and pay for your purchase over time. It's like getting a loan, but without having to go through the hassle of applying for one.

While this can be a helpful payment scheme for those who need a little extra time to pay off their big-ticket items, there are some things you should know before signing up. Namely, whether or not using BNPL will help improve your credit score.

Spoiler alert: it depends on how you use it. Keep reading to find out more.

Contents

- What is Buy Now, Pay Later (BNPL)?

- Can BNPL boost my credit score?

- How does BNPL work?

- Top 3 BNPL companies in the Philippines

- What are the cons of using BNPL as a payment method?

What is Buy Now, Pay Later (BNPL)?

BNPL or Buy Now, Pay Later is a type of financing that allows you to purchase an item and spread out the payments over a period of time. There are a handful of providers of this service in the Philippines, each with its own terms and conditions.

For example, some BNPL providers may offer interest-free financing for the short-term plan, while others may charge interest on the outstanding balance on top of your downpayment.

In general, BNPL lets you make larger purchases without having to pay for the full amount upfront. This can be especially beneficial for consumers who may not have access to traditional forms of credit such as credit cards.

When used responsibly, BNPL can help people manage their finances and make purchases they otherwise may not be able to afford.

Can BNPL boost my credit score?

If the BNPL loan provider submits the credit report to a credit bureau like Credit Information Corporation (CIC) that's in-charged of the credit scoring, it may affect the credit score. If you fail to settle dues on time repeatedly, this can affect your credit history.

Unlike traditional credit products like loans and credit cards, BNPL offers customers the ability to spread the cost of the item without too many requirements and documentation. Even without a credit history, you can avail of the payment scheme. It's important to check the terms and conditions of the BNPL before checking out.

If you're paying in full, and the BNPL loan provider is reporting it, this can show lenders that you're a responsible borrower. This is an advantage for those who don't have a credit history.

How does BNPL work?

Buy Now, Pay Later is a popular payment method among merchants, sellers, and online shoppers. It's also referred to as an installment payment. It works by creating a line of credit for the shopper. You set a period to pay off the purchase, typically two weeks or more.

Once the purchase is paid off, the line of credit is closed. If you don't pay it off within the agreed-upon timeframe, you will be charged interest and late fees, depending on the loan provider's terms and conditions.

To use BNPL, simply select it as your payment method at checkout when you shop on websites that support BNPL. You will need to connect your BNPL account or fill out a short form like name, date of birth, and other personal information.

Once this information is verified, you can complete your purchase and start paying the total amount due through local banks, e-wallets, and other supported modes of payment connected to the BNPL account. In a nutshell, you don't directly pay the merchant, but the BNPL loan provider serves as a conduit of the transaction.

BNPL is a convenient way to make big purchases without paying for them all at once. However, it's important to remember that BNPL is still a form of credit. You should only use it if you're confident that you can repay the balance on or before the due date.

Otherwise, you may end up paying more in interest and fees than you would have if you had paid for the purchase in full.

Top 3 BNPL companies in the Philippines

Here are popular Buy Now, Pay Later companies that allow you to pay for big-ticket items in stores and online.

Atome

Atome, a Singapore-based company, has extended its BNPL service to Filipino consumers. You can quickly sign up on your mobile device by downloading the Atome app on the Google Play Store and App Store for free.

Simply fill out the fields with your personal information and also link your local bank, e-wallet, or debit card as your mode of payment when settling bills.

Shop online and pay them in three easy plans without interest. The company has partnered with some of the biggest local brands, such as The SM Store, Watsons, Rustan's ZALORA, and Charles & Keith, to name a few. You can also book tickets and hotels through Agoda.

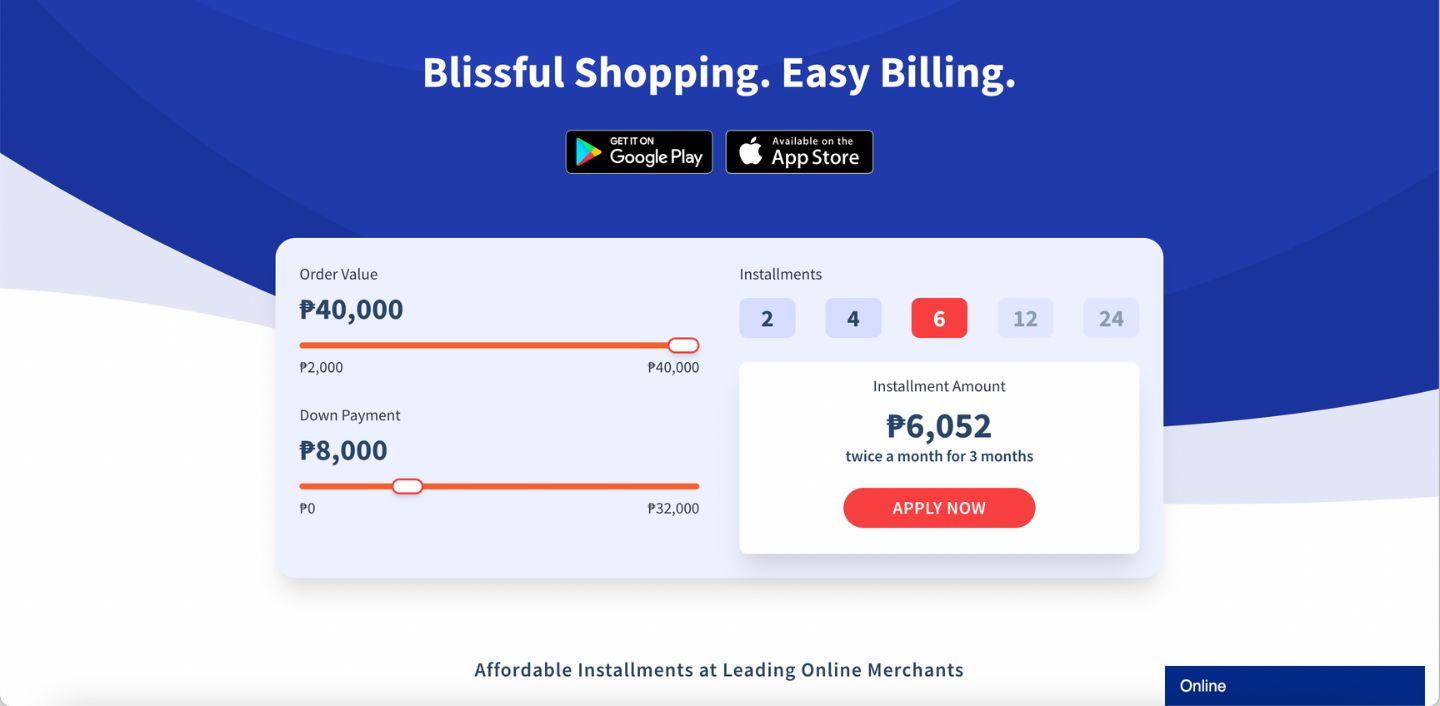

BillEase

BillEase is another top BNPL company in the Philippines with payment terms of 2, 4, and 6 months for new customers while 12 and 24 installments for repeat customers. With this BNPL company, you can pay a downpayment for your big purchases, and the rest will be financed.

Enjoy up to ₱40,000 of credit that you can use to pay merchants and online stores that accept BillEase as a mode of payment. The interest rate is at 3.49% per month, and you may also check out some of the partner merchants that offer 0% APR.

You need to sign up on the mobile app to get started and complete the verification process by submitting your personal information. You are required to submit one valid ID, proof of income, and proof of billing. BillEase decides your initial credit limit, so if you have a low limit, make sure you pay on time to build a good credit standing.

Plentina

Lastly, Plentina is another BNPL company that provides a credit limit for easy payments on groceries, medicine, bills, and fuel, to name a few. It's ideal for consumers who don't have a credit history. Thus with frequent use of the service, they can build a credit score.

This BNPL company requires you to sign up on its mobile app and complete the verification process. It's the one that also sets the credit limit of new customers, which serves as the virtual or electronic credit.

Plentina's repayment options are GrabPay and GCash. You may also pay over-the-counter at 7Eleven stores. The company has partnered with trusted local companies and merchants such as ZALORA, SouthStar Drug, National Bookstore, Lazada, Shopee, Smart, and Edamama, to name a few.

What are the cons of using BNPL as a payment method?

Although BNPL can be a convenient way to finance a purchase, there are also some potential drawbacks you need to keep in mind.

- You may pay more for your purchase - many BNPL schemes involve high monthly interest rates. Compare how much the item will cost if you pay it in full versus if paid in BNPL, and you'll be surprised by the interest charged even for a short-term repayment.

- You may miss out on rewards and perks - if you use a credit card to finance your purchase, you may be able to take advantage of rewards like cash back or points that can be redeemed for travel or other perks. With BNPL, you won't typically earn any rewards on your purchase.

- You could damage your credit score - if you don't make your payments on time or max out your BNPL limit, it could hurt your credit score. This could make it more difficult and expensive to borrow money in the future.

Final thoughts

In a nutshell, BNPL is a form of payment that allows consumers to purchase items now and pay for them in installments over time. This can be a great option for those who want the convenience of paying for goods in lighter payment terms but may not have the credit score or cash flow to get approved for a traditional credit card.

Does Buy Now, Pay Later boost your credit score? Yes, it does, that's why it's important to pay on time and use it responsibly whenever you shop online.

Have you ever used this payment method? What was your experience like? Could you share it with us in the comments below?