Are you looking for flexible payment terms and low rates for your home loan? If you plan to build your dream home, renovate an existing one, or refinance a property, here's a guide on BPI’s home loan rates and everything else it offers.

Overview of BPI Home Loan Philippines packages

As an established commercial bank, BPI offers competitive rates and flexible payment options.

The approval of the loan is not automatically guaranteed, though. Approval will be given based on a number of criteria. To facilitate a quicker loan approval process, make sure to submit complete documents and that you are eligible to apply for a loan.

Property Type: BPI Home Loan Home Acquisition

Fixing Period (years) | Rate (per annum) |

1-3 | 5.88% |

4-5 | 6.88% |

10 | 9.50% |

15 | 10.50% |

20 | 12.00% |

Property type: BPI Home Loan Construction & Renovation

Fixing Period (years) | Rate (per annum) |

1-3 | 5.88% |

4-5 | 6.88% |

10 | 9.50% |

15 | 10.50% |

20 | 12.00% |

Property type: BPI Home Loan Property Equity

Fixing Period (years) | Rate (per annum) |

1-3 | 6.88% |

4-5 | 7.88% |

Approved rates and fixing periods depend on the property that you will buy.

As of writing, home loan applicants can avail of down payment options for as low as 10%. However, this is still subject to home loan approval.

The lowest down payment rate that most commercial banks can offer is 10%. But remember that a low down payment means a bigger monthly amortization.

BPI Home Loans for Home Acquisition (Fixing period up to 20 years)

As of writing, BPI is offering three types of packages. But the packages for home acquisition and home construction and renovation share the same fixing periods and rates.

A 1-year fixed-rate home loan locks at a fixed rate of 5.88% for a period of 1 year. You can finance the following in this package:

- a residential lot

- house and lot

- residential condominium

- townhouse

- apartment

- residential building

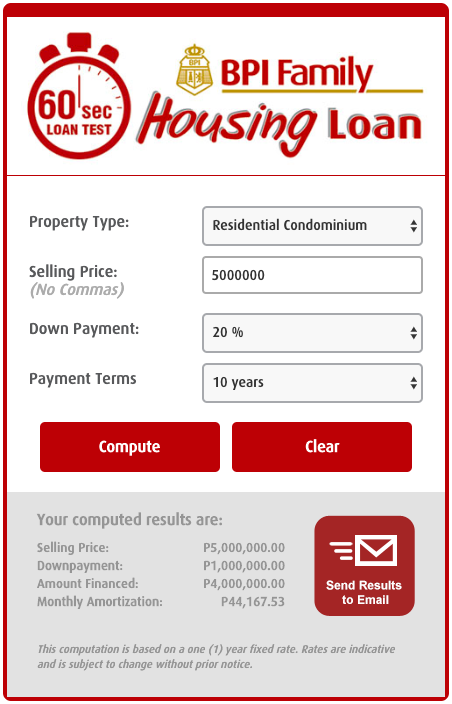

You can borrow a minimum of P400,000 based on the rates listed above. Here's a sample computation for a home loan to purchase a condo unit worth P5 million.

Image screenshot from BPI as of 27 February 2020

If you're buying a house and lot, you can borrow a maximum of 70% of its appraised value.

Meanwhile, for a vacant lot or residential condo unit, you can borrow a maximum of 60% of its appraised value.

If you're employed and the purpose of your loan is for owner occupancy, you can borrow up to 80% of the appraised value of the house and lot, provided it's not exceeding P5 million.

How long can you pay your BPI home loan?

The minimum loan tenure is 1 year, and the maximum is 25 years. If you’re borrowing money for a house and lot purchase, you can pay for up to 25 years.

Vacant lots, residential condo units, business loans, and refinancing can be up to a maximum of 10 years.

What are the eligibility requirements of a BPI home loan?

If you’re of legal age and not more than 65 years old upon the maturity of a home loan, you can submit your documents for home loan application.

Whether you’re a native Filipino, a foreigner married to a Filipino citizen, or a foreigner with issued immigrant or resident visa, you are eligible to apply (solely for the acquisition of a condominium unit only).

Each type of applicant is required to submit specific documentary requirements.

The minimum total household income for you to qualify for the home loan is P40,000.

For pre-processing requirements, you must submit the home application together with the income documents and collateral documents.

What are the documentary requirements for BPI home loan application?

Here are the documents you need to submit together with your duly accomplished home loan application and two valid IDs.

If you’re married, both spouses should fill out the form. Meanwhile, forms need to be filled out separately if you have a co-mortgagor.

Locally employed (within the Philippines) | Self-employed | Expat Pinoy (OFW) |

|

|

|

If you’re a practicing doctor, submit the clinic address(es) and schedule. If you’re from a commission, send vouchers or bank statements showing the last 6 months reflecting your commission income.

If your income is from rental and lease of properties, submit the following:

- Rental/Lease Contract (indicating name of tenants and rental amounts with complete addresses of properties being rented)

- Photocopy of Title (TCT/CCT)

For collateral documents and other information, visit the BPI Checklist Requirements page.

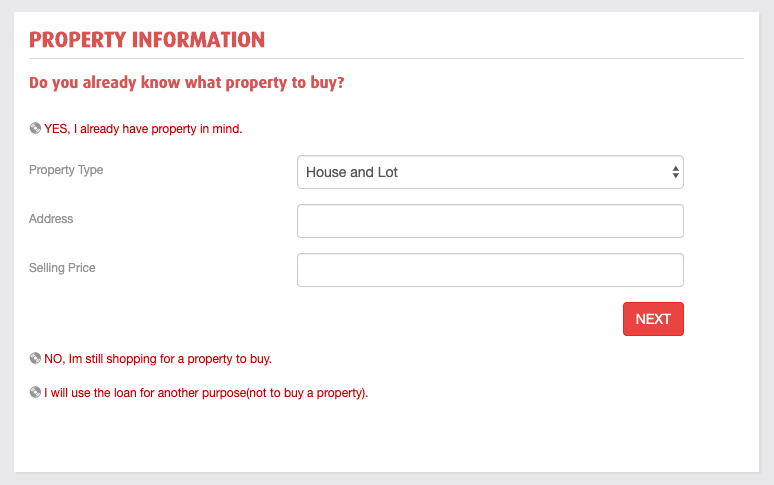

How to apply for a BPI home loan in the Philippines?

Visit the online portal and follow the three-step process, filling out the online forms with your details.

Fill in the details about property information, borrower information, and the submission page.

If your application is submitted outside the standard working hours (8:30 AM - 5:30 PM), it will be processed on the next business day.

If you prefer to speak with a banking officer, you can visit your nearest BPI branch or refer to the following communication channels and contact numbers:

- For Housing Loan Accounts - (02) 889-10000, option 4-4-0

- Or text HOUSING[SPACE]NAME[SPACE]MESSAGE and send to 0917-891-0000

- Email BPI: New Housing Loan Applications - [email protected]

- Existing Housing Loan Accounts - [email protected]

Image screenshot from BPI website 27 February 2020

Is the BPI Home loan for you?

A home loan is a major financial commitment. Make sure that you can afford to pay for the monthly amortization before signing any contracts.

If you’re thinking of borrowing money for property acquisition, BPI offers a minimum loanable amount of P400,000 and a maximum of up to 70% of the appraised value.

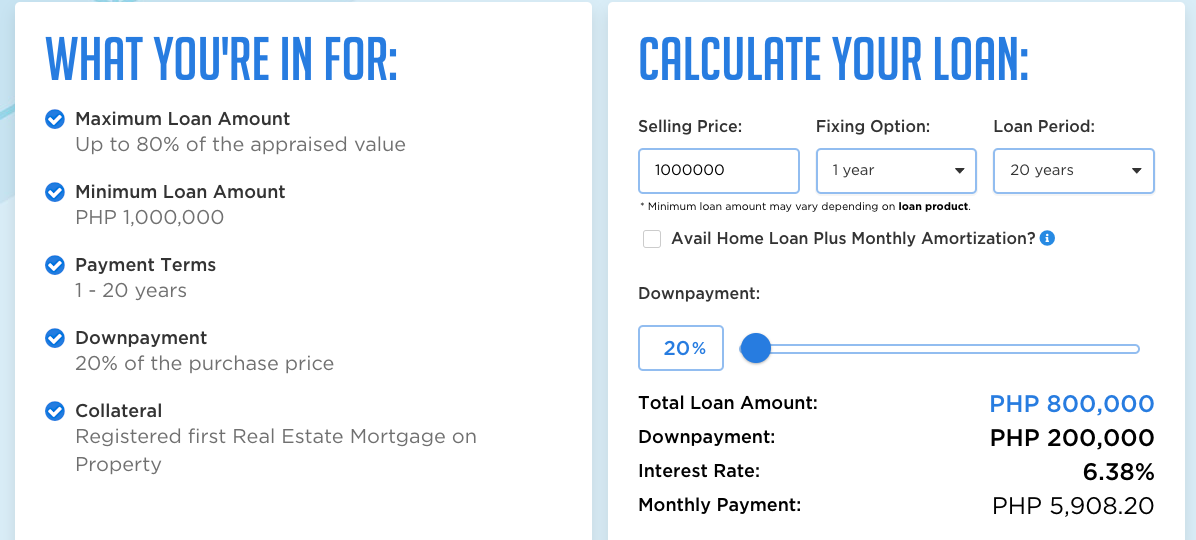

We also reviewed RCBC Home Loan rates for property acquisition where the minimum loanable amount is P1,000,000 and the maximum is up to 80% of the appraised value.

Image screenshot from RCBC as of 27 February 2020

BPI is a good option for those who want to take out a loan to acquire a property for P400,000 or lower.

If you will also compare BPI’s 1-year fixed period for home loan acquisition to RCBC’s, BPI offers a better rate at 5.88% to RCBC’s rate of 6.38% (based on the sample calculator above. Keep in mind, though, that these are sample computation and the actual monthly payments may vary.

Do you see yourself paying for your acquired home for up to 20 years? Let us know what you think of the BPI home loan in the comments below.