Thanks to digital banks like CIMB Bank, SeaBank, GoTyme Bank, and Maya Bank (formerly PayMaya), opening a savings account takes about ten minutes or less. Even traditional banks like Maybank, UnionBank, and RCBC have upgraded their registration processes—all these can be done through your smartphone.

Fun fact: In a survey conducted in the fourth quarter of 2023, banks dominated as the go-to savings choice for 73.5% of surveyed Filipino households. Surprisingly, 55% of those surveyed preferred stashing cash at home. I also learned that based on Banko Sentral’s report in 2017, 62% of depositors only keep less than ₱5,000 in their balances.

I’m pretty sure you want more than ₱5,000 in your account. If you’re looking for ways to save money and earn interest per annum, I’ll walk you through the current interest rates of these ten digital banks in the Philippines. I’ll also unpack some features and services to help you choose the right bank for your financial goals.

Overview of digital banks in the Philippines

Bank | Interest Rate Per Annum |

0.50% - 2.60% | |

5.00% | |

4.00% | |

2.50% | |

0.25% | |

3.50% — 14.00% | |

6.50% | |

4.50% | |

Up to 6.00% | |

6.50% |

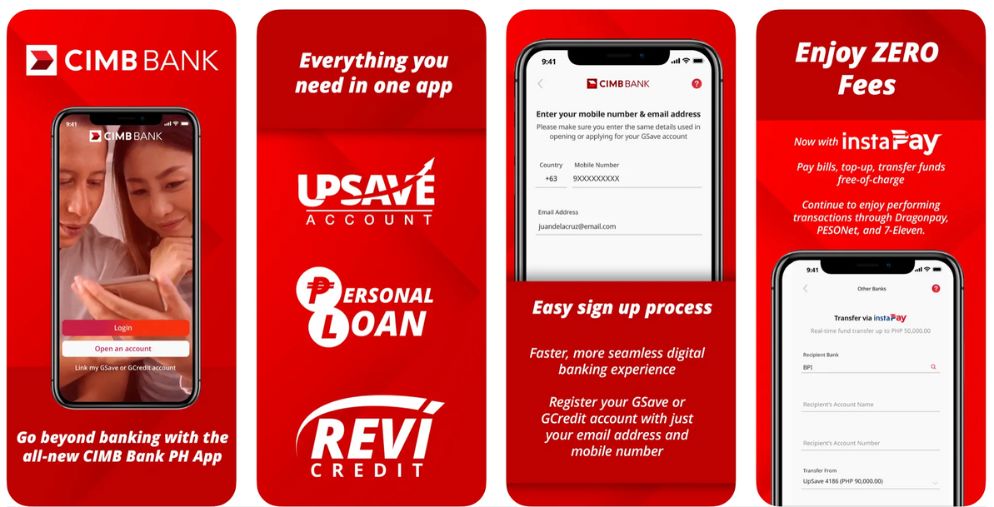

CIMB Bank — Great for frequent GCash users

Image: App Store

CIMB Bank Philippines is an all-digital mobile bank. Its first financial product was GSave, which the bank integrated into the GCash app. Eventually, the company introduced other savings accounts, like Upsave, Fast, and Fast Plus, that offer annual interest rates from 0.75% to 2.6%.

Open your account from the mobile app and choose the savings account that best suits your financial goals. Here are the three major savings accounts to choose from:

- Fast Plus: an entry-level current account with a VISA debit card offering a 0.75% annual interest rate.

- Upsave: earn 2.50% interest p.a., no minimum deposit required and maintaining balance, and comes with complimentary life insurance with up to ₱250,000 if you keep a minimum average daily balance of ₱5,000.

- GSave: accessible in the GCash app and offers a 2.60% interest rate per annum. You can also transfer GCash funds to the GSave account without fees.

Top up your CIMB account via bank transfers and through more than 8,000 partners, including 7-Eleven, SM Payment Center, and LBC.

If you frequently use GCash, you’ll find CIMB more convenient for transferring funds from your account to your wallet and vice versa. Deposits and withdrawals can be made through 7-Eleven stores and major banks, and this is worth keeping for short—and long-term savings.

BPI BanKo — Great self-employed and micro-entrepreneurs

Image: App Store

BPI BanKo is the digital bank of the Bank of the Philippine Islands that focuses on providing financial services to self-employed and micro-entrepreneurs. Like most digital banks, you can open a savings account, pay bills, and send and receive funds. What’s unique about this digital bank is that you can apply for business loans of up to ₱500,000.

Here are some of the features that will also convince you to open an account:

- Todo Savings account lets you earn up to 5.00% per annum for balances ranging between ₱5,000 to ₱1 million.

- No initial deposit is required if you open the PondoKo SEME, but you need to maintain a minimum of ₱5,000 daily to earn interest.

- No maintaining balance is required if you open a PondoKo Basic account The overall language is Taglish (Tagalog-English), making it more accessible and inclusive to Filipinos to understand financial terminologies.

- NegosyoKo Loan, a lending feature, lets small businesses borrow money from ₱25,000 up to ₱500,000.

- Get a 2% rebate when you top up your mobile prepaid number to all networks.

BPI BanKo’s high-interest savings account, TodoSavings, offers a good deal for savers—it competes with CIMB, SeaBank, Tonik, and Maya Bank. However, if you exceed ₱1 million in your account, you will only earn 0.0625%. The mobile app has a decent user interface but requires more updates, as some users rant about the app's crashes and performance.

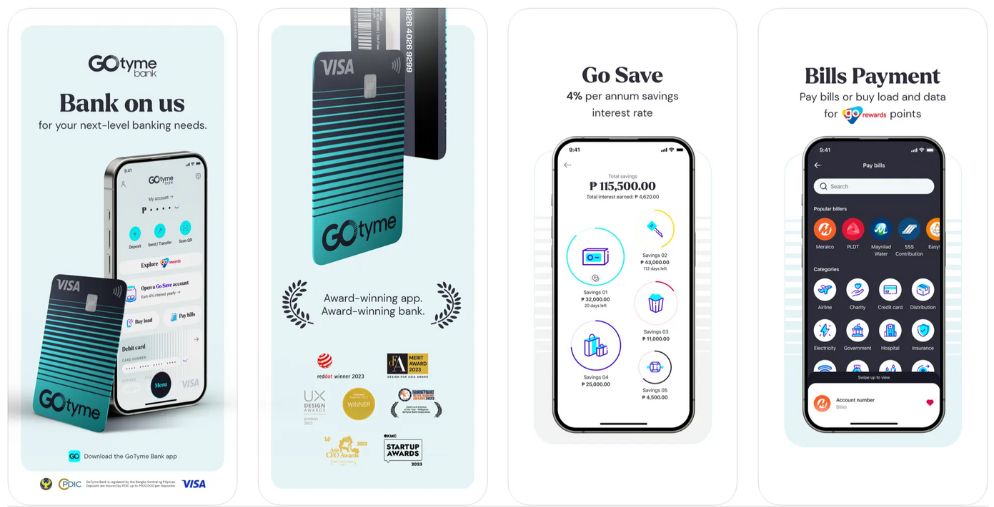

GoTyme Bank — Great for shopaholics who want cash rebates

Image: App Store

GoTyme is one of the digital banks in the Philippines that promotes the phygital banking experience, combining the physical and digital elements in its core services. GoTyme is a joint venture between the members of Gokongwei Group in the Philippines and Tyme, a digital banking group from South Africa.

GoTyme’s savings account offers 4.00% p.a. and uses a reward system where you can earn points to redeem cash. Here are the other features of this digital bank:

- Set up an account using the mobile app and get your personalized metallic-sheened VISA debit card for free at any physical kiosks in Robinsons supermarkets.

- Earn up to 3X points when you use the debit card to pay for partner brands and stores that accept Go Rewards, like Robinsons Supermarket, Daiso, The Marketplace, Toys R’Us, and Shopwise, to name a few.

- Pay bills and top up your prepaid number to earn GoRewards.

- Enjoy three free bank transfers every week — from your GoTyme account to other banks via InstaPay.

- Create up to five separate Go Save accounts and customize your goals for saving funds.

I opened a GoTyme account, and I think it’s useful if you’re shopping on most Robinsons-owned brands like The Marketplace, Toys R’Us, Handyman, TrueValue, and more. It’s a debit card for moms and dads who want to track their expenses and prefer to use debit than credit cards. The interest is credited to your account every first day of the month. If you love to budget your funds while earning redeemable points for cash, opening a savings account is worth it.

? Download on the App Store ? Download on the Google Play Store

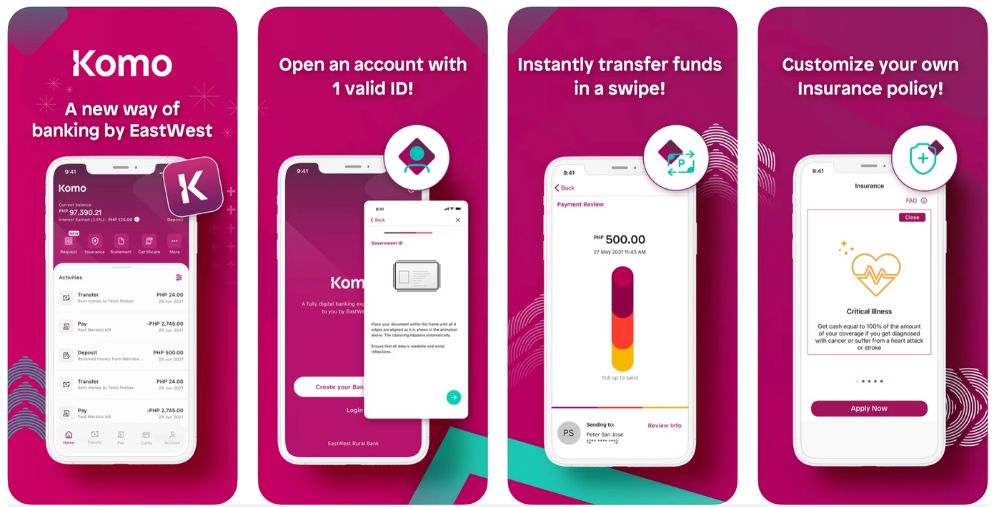

Komo Bank — Great for budgeting and managing short-term savings

Image: App Store

If you want your savings to be associated with and backed by an established commercial bank like EastWest Bank, Komo Bank is a good option. This digital bank emphasizes the concept of “you being in control,” thus the name “Komo” “Kontrol mo ang pera mo.” Sounds cheesy for some, but a 2.50% p.a. is a fair offer.

Here’s what to expect from this digital bank:

- No minimum deposit requirements.

- Earn 2.50% p.a. With no maintaining balance.

- Send as much as ₱250,000 per day (₱50,000 per transaction) to other bank accounts.

- Free VISA debit card delivered to your address.

- Pay bills, send money to other banks, and withdraw cash for free within the EastWest network.

- Analytics feature gives you an overview of how you spend money.

- Goals feature lets you set a budget for short and long-term funds.

Komo Bank is your typical digital bank with the basics—without the bells and whistles like complicated bonus offers to earn high interest rates. Some users praise its clean and straightforward user interface, which I agree with.

If you’re an analytical and organized saver, you will appreciate the Analytics, which gives you more insights on deposits and expenses.

Maybank2U PH — Great for frequent travelers

Image: App Store

Maybank launched iSave, its first online-only savings account, through the mobile app. You can open a savings account straight from your phone and submit the documents online.

This digital bank offers basic banking services like:

- No initial deposit or minimum balance is required

- Earn a profit of 0.25% per annum as long as you have ₱20,000 as your average daily balance.

- Deposit up to ₱100,000 in your account, and you will also receive an EMV-enabled ATM card if you top up your account with a one-time deposit of at least P1,000.

- Fund your account via Maybank branches, GCash wallet, mobile bank transfer, and over-the-counter outlets such as 7-Eleven, Tambunting Pawnshop, and USSC, to name a few.

- When in Singapore, Malaysia, and Cambodia, you can withdraw from any Maybank ATM with your debit card, with zero transaction fee and a low conversion rate.

There’s nothing much to say about this digital bank's features and services except that if you’re a frequent traveler in Singapore, Malaysia, and Cambodia, you can use the debit card for overseas transactions. The interest rate is lower than what other digital banks offer, so this may be a dealbreaker for some.

Maya Bank (formerly PayMaya) — Great for online transactions

Image: App Store

Maya Bank, formerly PayMaya, is a fully digital bank that offers a base rate of 3.50% p.a. and a promotional offer of up to 13.00%. To earn higher interest rates, you complete specific tasks that earn you 1% p.a. to 2.00 p.a. %, referred to as Boosts — pay bills via QR card, pay a merchant, or checkout items at Maya Shop.

Looking inside the Maya Bank app can be overwhelming for those who need to be digitally savvy. I’ll only highlight the ones related to savings:

- Personal Goals feature is like a time deposit account where you can save up for your plans and earn 4.00% p.a. for six months based on your average daily balance of up to ₱1 million.

- Send and receive money from other banks using the QR PH code.

- Comes with a virtual card that you can use for online purchases.

- Transfer funds to other wallets like GCash.

- Supports bill payments and purchases of mobile load.

If you love keeping tabs on your expenses and paying cash, you can use the Boosts to complete the tasks and earn higher interest rates. Things can be complicated for those who want to put their funds into growing it without being too hands-on. Maya Bank wants to keep you in its ecosystem — save, spend, earn, and repeat.

RCBC DiskaTech Savings — Great for beginners

Image: App Store

Image: App Store

RCBC DiskarTech is a digital bank in the Philippines offering inclusive financial services through a mobile app in TagLish and Cebuano. This makes banking more accessible to Filipinos in all walks of life.

With a 6.50% interest rate p.a., you can grow your savings without minimum deposits, maintaining balance, or dormancy fees. The interest rate is quite competitive, allowing unbanked people to open an account and save more.

However, upon checking the features and services, you might find some deal breakers.

- The account limit is set to ₱47,900 only for a full basic deposit account, which allows savers to earn 6.50% p.a., which includes the interest, so technically, the account will only have ₱50,000.

- If the balance exceeds the net savings of ₱47,900, savers won’t earn any interest. The maximum account for deposit per transaction is ₱25,000, and they are only allowed twice daily.

- Cash-ins and deposits to the savings account are available at 7-Eleven stores, Bayad Centers, and Cebuana Lhuillier, to name a few.

- Account holders can apply for a loan at RCBC DiskarTech partners like Asialink Finance Corporation and Rizal Microbank.

If you frequently transfer funds, you might be better off with other digital banks. Basic online banking features are available, including bill payments and airtime load top-up. Other than these, the account limits on transfers and balances are dealbreakers.

SeaBank — Great for savings for long-term

Image: App Store

SeaBank by SeaBank Philippines is another digital bank regulated by the Banko Sentral ng Pilipinas. There’s no minimum balance to maintain your account, no deposit cap, and no lock-in period. You can deposit as low as ₱1 and start growing your money with its 4.50% interest rate per annum.

Here are some of the features and services worth mentioning:

- Depositors receive a daily payout of the interest earnings, 4.50% p.a. for balances up to ₱350,000 only, and 3.00% p.a. above that amount.

- Easily connect your account with the Shopee app for easy top of your ShopeePay account.

- Send funds to major e-wallets, such as GCash, Maya, GrabPay, COINS.PH, and the Lazada wallet.

- Supports a doze of billers for utilities and credit cards and lets you top up prepaid mobile numbers with 3% rebate for Globe, Smart, TM/TNT, and DITO.

- Transfer money to other banks via InstaPay and PESONet. The maximum amount you can transfer per transaction is ₱1 million if you transfer to another SeaBank account or via PESONet.

- The maximum amount per transaction for InstaPay is ₱50,000 per day.

I personally have a SeaBank account. It used to offer up to 5.00% p.a. Interest rates, but they have decreased them to 4.50% p.a. What I like about this is the daily crediting of earnings, which gives you that dopamine effect, seeing your money grow each day.

However, the only caveat I see here is that since it’s easily linkable to ShopeePay, it’s easy to spend the hard-earned money if you’re struggling with impulse buying. On Shopee, it’s easy to top up your wallet from SeaBank, so make sure you map out a budget for online shopping to avoid overspending.

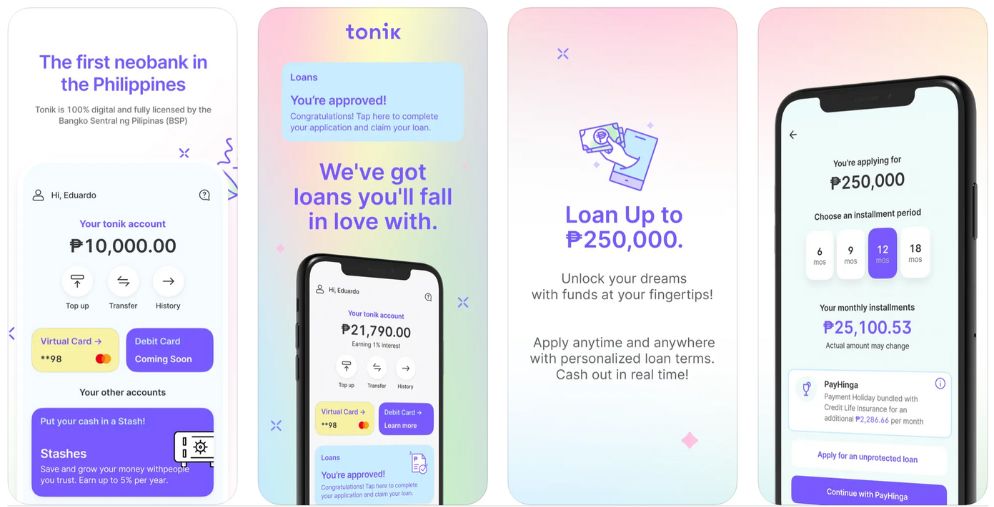

Tonik Digital Bank — Great for time deposits

Image: App Store

Tonik Digital Bank offers a full suite of banking services, including deposits, payments, debit cards, and loans. There are no minimum balance requirements. You'll earn interest on your deposits up to 6.00% per annum, and you can set your savings goals through the Stashes or separate savings pockets.

Here are some of the features to expect from this digital bank:

- Separate savings pockets where users can save money solo or in a group, with interest rates up to 4.5% per annum for Group Stashes.

- Offers deposit interest rates of up to 6.00% p.a. for time deposits up to six months only and with a maximum cap of ₱100,000 balance. Apart from this, you can also take advantage of the interest, ranging from 4.50% to 5.25%, with a holding period of up to 24 months.

- Comes with a virtual Mastercard debit card, which is issued upon onboarding or signup — it’s useful for online shopping and bills payments.

- Account holders can borrow money from ₱5,000 to ₱50,000.

Tonik’s offers are relatively reasonable, especially with the time deposits interest rates. If you’re planning to hold off your funds for more than six months, having a stash in this bank is a good option.

The brand’s voice does seem a bit off and out of context in the banking industry, according to some users who aired their concerns in a Reddit thread, given that its language is more informal, targeting Gen Zs and millennials. Others think it’s unprofessional to use a funky writing style.

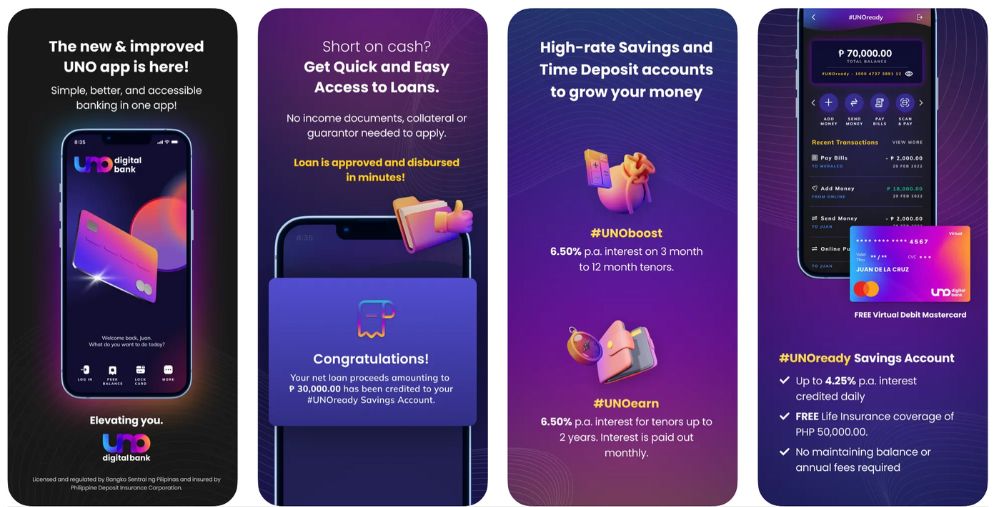

UnoBank Digital Bank — Great for savings and loans

Image: App Store

UnoBank Philippines, officially known as UNO Digital Bank, is a new entity in the digital banking space in the Philippines, licensed and regulated by the Bangko Sentral ng Pilipinas (BSP). The bank's innovative features include the numberless card, competitive interest rates, and commitment to security.

If you’re using GCash, you will see UnoBank featured on the app, prompting you to create a savings account. You can link your bank account to the e-wallet and earn interest rates annually.

Here are some of the features worth mentioning:

- UnoBank has partnered with GCash to offer a range of financial products and services, making it easier for users to manage their finances through the GCash platform.

- Get up to 4.25% p.a. with daily crediting, no minimum balance needed, no holding period, and free ₱50,000 life insurance for a monthly Average Daily Balance (ADB) of ₱10,000.

- Provides a guaranteed 6.50% p.a interest rate with up to 24 months tenure and monthly payouts.

- Seamless and free cash-in and cash-out transactions via GCash are available for convenient transfers.

- Provides collateral-free loans up to ₱200,000 with the flexibility of monthly installment payments for up to 36 months.

As the new kid on the digital banking block, UnoBank offers competitive interest rates on savings and time deposit accounts. If you have extra funds and aim to save them for six months or more, this is a good choice, aside from CIMB.

I recently signed up for a new account, but it keeps crashing during verification, such as submitting a valid ID and facial recognition. I’m not alone in experiencing this, as other users have also reported issues with the digital banking app, including lagging and problems opening the GCash app when UNO is opened.

Which digital bank is for you?

GoTyme, Maya Bank, and Tonik Bank offer higher interest rates on savings accounts and time deposits than traditional banks. Imagine you can grow your savings with their offer of up to 6.50% p.a. interest rate. The caveat is that each digital bank has limitations like a deposit cap on Tonik and requirements to complete tasks on Maya Bank to earn interest rates.

These are fully digital banks and provide convenient ways to transact online. Bills payments and fund transfers can be done through their respective mobile apps.

If you’re geared towards traditional banks with physical branches, Maybank can cater both online and over-the-counter account openings. GoTyme embraces a phygital experience that allows you to open an account on your mobile app and enjoy self-service via the physical kiosks available in Robinsons.

SeaBank and UNO Digital bank do have something in common — your earnings are credited to your account every day. If this is something that will help you save more, just choose any of the two that you think gives you more convenience in e-wallets and bank transfers.

Which of these digital banks do you want to use for the long term?

Let us know in the comments below.