If you’re a regular GCash user, you probably have seen UNO Digital Bank ads on your screen, prompting you to open a new savings account. Like you, I was curious about this digital bank that offers high interest rates on savings and time deposit accounts.

Uno offers its time deposit interest rate at 5.75% p.a., which is better than GoTyme, CIMB, SeaBank, and other digital banks in the Philippines.

But is there a catch? I’ve done the legwork for you and set up a savings account to see its features and benefits. Read further for this honest review.

Contents

- What is UNO Digital Bank?

- What are the key features of UNO Digital Bank?

- UNO Digital Bank app review

- UNO Digital Bank savings account interest rate vs. other banks

- What are the requirements to open a UNO Digital Bank account?

UNO Digital Bank savings account features

Type of Account | Peso Account |

Interest rate for savings account #UNOready | → Base interest rate (balances ₱0.01–₱4,999.99): 3.00% p.a. → Higher tier (₱5,000–₱4,999,999.99): 3.50% p.a. → Balances ₱5,000,000 and above: 1.00% p.a. |

Interest rate for a time deposit #UNOboost | → 3 to 5 months: 4.00% per annum → 6 to 9 months: 4.25% per annum → 10 to 11 months: 4.50% per annum → 12 months: 5.75% per annum |

Initial deposit | Zero |

Minimum balance required | None |

Maintaining balance required to earn interest | None |

Virtual debit card | Yes (₱100) |

ATM withdrawals | Yes |

ATM card | Mastercard (₱300) |

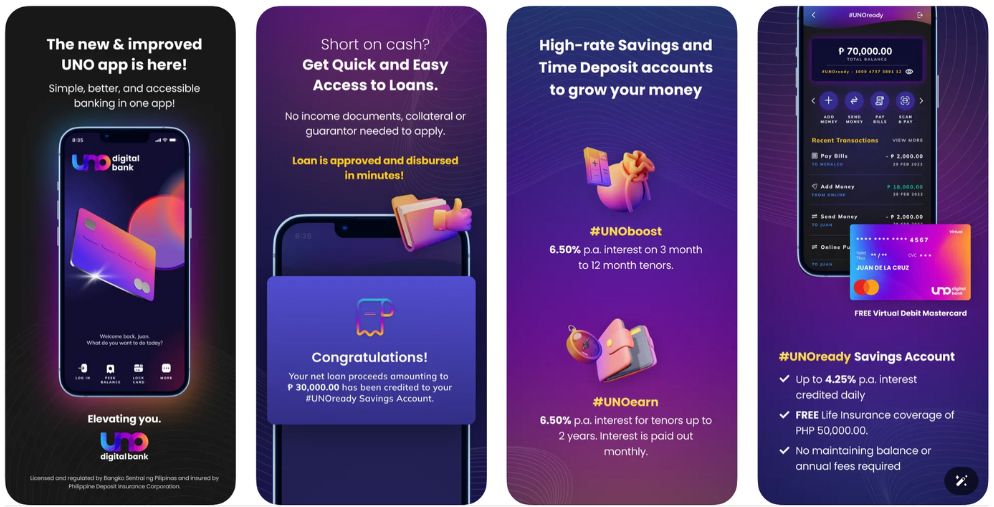

What is UNO Digital Bank?

UNO Digital Bank, licensed and regulated by the Bangko Sentral ng Pilipinas, is one of the pioneering neo-banks that has secured a digital banking license directly. The bank's offerings—including savings accounts, time deposits, and loans—are digitally accessible, facilitating everyday transactions and providing platforms for savings and investments.

To reach more consumers, UNO Digital Bank has partnered with GCash, one of the leading e-wallets in the Philippines. GCash's GSave feature integrates services from UNO Digital Bank through this collaboration. This allows GCash users to open a UNO Digital Bank account within the app.

What are the key features of UNO Digital Bank?

As a new player in the market, UNO Digital Bank still offers the security of PDIC coverage up to ₱500,000. But beyond that, its standout features make it worth considering for your next account.

1. Full spectrum banking services

UNO Digital Bank offers a full spectrum of banking services, including savings accounts, time deposits, personal loans, and the ability to pay bills, all accessible through its mobile app. This benefits users looking to manage their finances in a one-stop digital platform.

2. High interest rates on savings and time deposits

UNO Digital Bank offers attractive interest rates for savings and time deposit accounts. Let me unpack these three savings account offers:

#UNOboost time deposit

The #UNOboost time deposit account allows you to earn up to 5.75% p.a at maturity, with flexible terms ranging from 3 to 12 months. This feature particularly appeals to savers looking for higher returns on their time deposits.

A longer holding-off period means lower interest rates.

#UNOready regular savings account

For the regular savings account, you have two options to earn more. If funds are below ₱5,000, you earn 3.00% p.a. Otherwise, if you deposit more than ₱5,000, you earn 3.50% p.a. For deposits of ₱5 million and above, you only earn 1.00%.

One thing I noticed about the offerings is that you must be vigilant to spot tricky terms and conditions, as the promos and offers vary depending on how much you’re saving up in your account.

The good news is that UNO Digital Bank gives you daily payouts, just like SeaBank does. Plus, if you have a regular savings account, you get a free ₱50,000 worth of life insurance coverage.

Here’s a breakdown of the interest rates and corresponding deposits.

End-of-day balance | Gross interest rate | |

From | To | |

₱0.01 | ₱4,999.99 | 3.00% |

₱5,000.00 | ₱4,999,999.99 | 3.50% |

₱5,000,000.00 | Above ₱5 million | 1.00% |

#UNOearn and #UNOboost via GCash

You can also sign up or open a savings account through the GCash app, and you can choose between the two savings account offers:

#UNOearn

- Guaranteed 5.00% p.a. interest rate. This product offers a fixed interest rate of 5.00% p.a., which means that the rate is guaranteed and does not fluctuate over the tenure of the time deposit.

- Up to 24 months tenure. Customers can choose to lock in their funds for a period of up to 24 months, providing a longer-term saving option.

- Monthly payouts. Interest earned on the deposit is paid out monthly, which can be an attractive feature for those looking for a regular income stream from their deposits.

#UNOboost

- Up to 5.75% p.a. interest p.a. Similar to #UNOearn, this product also offers an interest rate of up to 5.75% p.a.

- 3 to 12 months tenure. The tenure options are shorter, ranging from 3 to 12 months. This provides more flexibility for customers who may want to wait to commit their funds for as long as two years.

- Payout at maturity. Unlike the monthly payouts of #UNOearn, the interest for #UNOboost is paid out at the end of the term, at maturity. This could be more suitable for those who do not need periodic income and prefer to have the interest compounded until the end of the deposit period.

3. All digital account opening process

Opening an account with UNO Digital Bank is streamlined and can be completed in less than 15 minutes. Only a valid government-issued ID is required for verification.

This process is significantly faster and more convenient than traditional banking, where account opening can take much longer and may require a visit to a branch.

One of the things I noticed when I opened an account was that there were quite a few glitches and lags.

I guess they’re still working on the app’s performance, which can be cumbersome—although if you’re filling out the form, the mobile app has already saved the previous entries, so you don’t have to fill out your details again.

4. Accessible loan product with #UNOnow

UNO Digital Bank offers a #UNOnow loan product to provide quick and accessible financial assistance. Eligible loan applicants with a minimum gross income of ₱20,000 can borrow from ₱10,000 to ₱250,000.

According to my research, some partners quote up to ₱500,000 based on the borrower's profile.

Here’s what I’ve found about this loan product:

- No collateral required. One of the most appealing aspects of the #UNOnow loan is that it does not require any collateral. This feature makes it accessible to a broader range of customers, including those who may not have assets to offer as security for a loan. With fewer documentation requirements, you can submit contact details, a valid government-issued ID, and a selfie as part of the application.

- Repayment tenure. The loan offers flexible repayment options with tenures ranging from 6 to 36 months. This flexibility allows you to choose a repayment plan that fits your financial situation and capacity.

- Competitive interest rates. The monthly add-on interest rate starts at 1.79%. The annual percentage rate ranges from 35.78% to 37.54%, depending on the loan tenure.

Loan Terms

Feature | Detail |

|---|---|

Amount | ₱15,000 – ₱250,000 |

Tenure | 6–60 months |

Monthly Add-On Rate | 1.79% (lowest) |

APR | 35.78% – 37.54% (depending on the tenor |

Disbursement Time | As fast as 20 minutes post-approval |

Eligibility Requirements

- Age: 21–65 years old (at loan maturity)

- Locations: Metro Manila, Cebu, Rizal, Cavite, Laguna, +20 other provinces/cities

- Income Proof:

- Employed: Payslips + bank statements (avg. ₱10,000 balance)

- Self-employed: DTI/Mayor’s Permit + financial docs

For real-time verification, you can check UNO’s loan calculator.

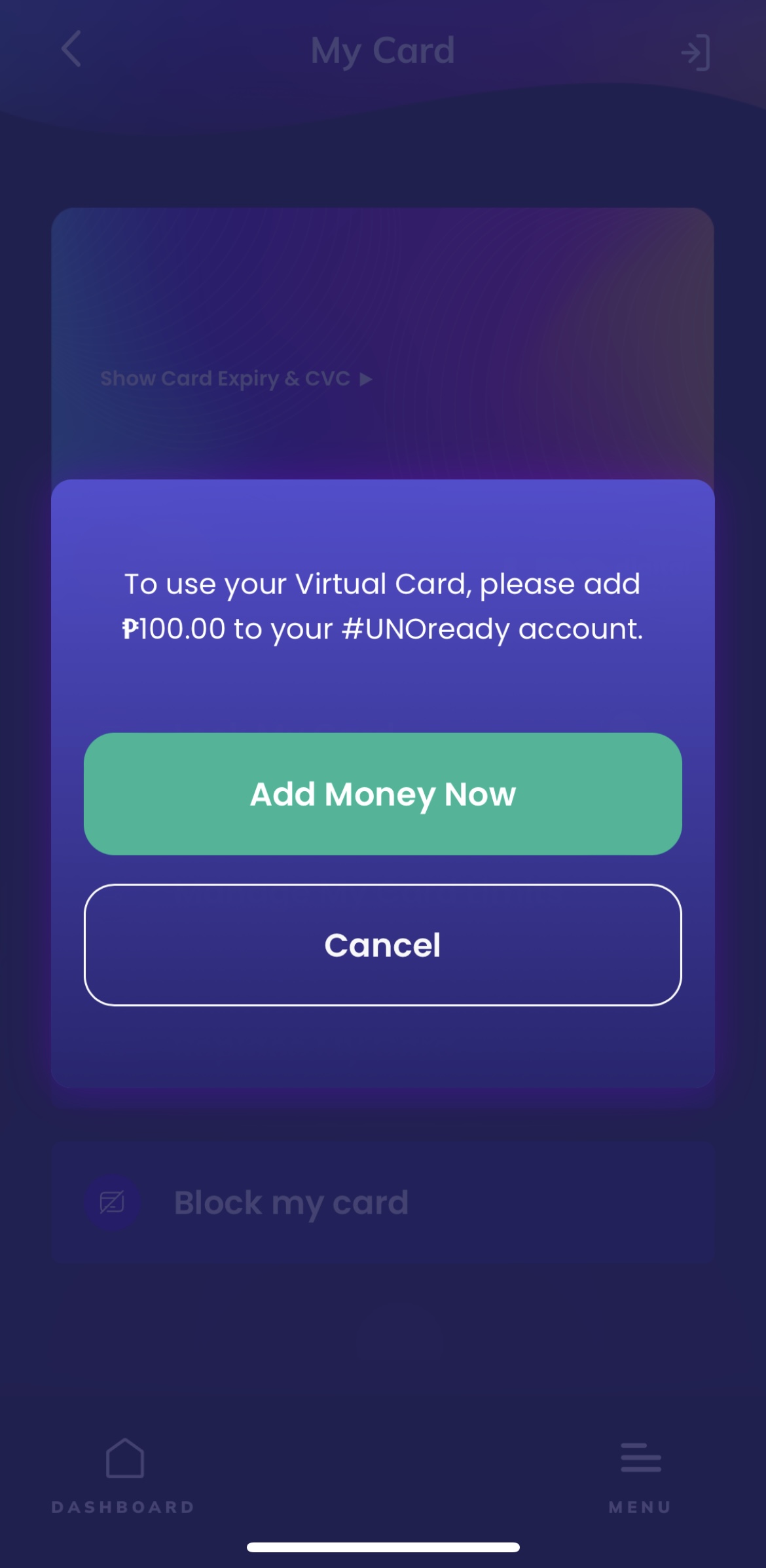

5. Virtual debit card

Upon opening an account, you automatically receive a virtual debit card, which can be used for online transactions worldwide.

You need to top up ₱100 to activate it—this card enhances the digital banking experience by providing a secure and convenient way to shop online.

UNO digital bank app review

I tried the digital bank myself so I could experience it and provide an objective review. I found a few things that are quite a nuisance for the user experience, and also some good points to keep in mind.

1. Login and authentication

The app provides both biometric login, which includes Face ID, and password authentication. This kind of security is great to make sure no one else can access my account. But sometimes there are hiccups and lagging when I log in.

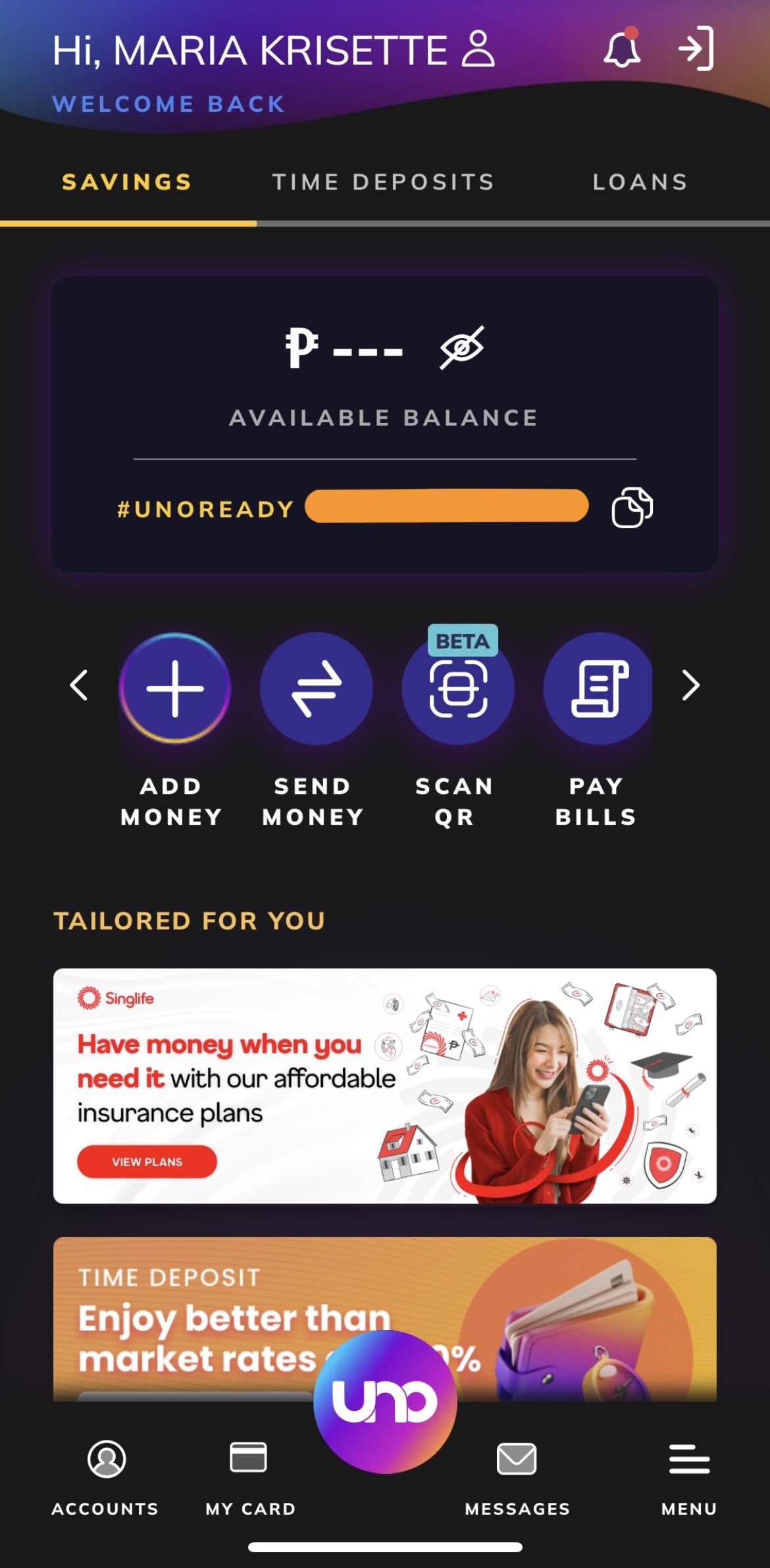

2. Dashboard and navigation layout

The main dashboard is all inclusive with navigation tabs for savings, time deposits, and loans. Available balance is at the opening page, which is helpful for quick referencing. That’s a plus point for me because I can easily access these main services or offerings.

Apart from these, there are multiple action buttons, with:

- Pay bills

- Insurance options

- QR code scanning

- Cash withdrawal features

3. Performance issues

I have faced several performance issues that directly affect the end user experience likie the specks of hiccups that become trapped on the screen noticed the delay when I tap some icons. Sometimes I get a bug or two in selecting certain options and annoying navigation issue where pressing the back button some times completely signs me out.

4. Interface redundancy

The app appears to be duplicating functionality in several places. For instance:

- "Add money" "Send money" options are clearly visible on the dashboard and the main button menu on the bottom.

- Things like scan QR code, pay bills, and get cash have similar duplication.

This redundancy leaves me slightly confused as to where to go. It feels like an effort to put all options in one screen only to muddle the entire UI/UX experience.

5. UNO Gen AI Chatbot

The chatbot is also an interesting addition, which is located on the right upper corner—it will pop up when you tap it.

But this “UNO Gen AI” does take some few seconds to load up so that you can chat with them. You can ask it questions or for a specific bit of information, and it does a fair job of giving information about bank services.

An honest review and overall impression

The app feels like it’s attempting to offer a more complete bank experience, but it’s crumbly execution.

Performance lags, redundant interface elements and the sometimes obtrusive delay on switching from one option to another that’s a pain for the navigation.

UNO Digital Bank savings account interest rate vs. other banks

Here’s a comparison of the UNO Digital Bank interest rate versus other banks. I know there are quite a few digital banks out there that offer higher p.a. Interest rates, may this table give you a concrete view of the offers.

Bank | Interest Rate p.a. (per annum) | Minimum Initial Deposit (depending on the type of Savings Account) |

UNO Digital Bank | 3.00% — 5.75% | None |

Digital banks in the Philippines | ||

0.50% – 0.75% Fast & Fast Plus Account2.50% UpSave Account2.60% GSave Account | None | |

3.50% (Go Save) | None | |

2.50% - 3.00% | None | |

3.5% (base rate) | None | |

3.50% - 4.5.00% | None | |

1.00% (Regular)4.00% (Stashes) | None | |

Traditional commercial banks in the Philippines | ||

0.0625% | ₱100 – ₱30,000 + | |

0.0625% to 0.125% | ₱100 – ₱2 million | |

0.125% | ₱2,000 -₱20,000 + | |

0.75% to 2.04% | ₱50,000 – ₱2 million | |

0.0625% | ₱5,000 -₱100,000 + | |

What are the requirements to open a UNO Digital Bank savings account?

To open a UNO Digital Bank savings account, the requirements are as follows:

- Age requirement. You must be at least 18 years old.

- Residency. You need to be a resident citizen of the Philippines.

- Address. You must have a present and/or permanent address in the Philippines.

- Identification. You need at least one (1) valid government-issued identification document (ID).

- Email and mobile number. You must have a valid email address and local Philippine mobile number.

The process involves downloading the UNO Digital Bank app, registering with your mobile number, verifying your identity through ID and facial scan, and setting up your password and passcode.

Final thoughts

UNO Digital Bank could be recommended for individuals who are comfortable with managing their finances through a mobile app and are looking for higher interest rates on savings and time deposits compared to traditional banks.

It may also appeal to those who need quick access to loans without collateral. The integration with GCash makes it a convenient option for existing GCash users to conveniently transfer funds to and from their e-wallets to UNO savings accounts.

Based on my research, the app has received mixed reviews regarding customer service responsiveness to these issues. The bank's digital nature means that if you prefer in-person banking experiences or are not tech-savvy, you may find it less suitable, even if it offers high p.a. interest rates.

Have you tried UNO Digital Bank? Share your thoughts and experiences in the comments below.

Want more content like this? Don't forget to follow Moneysmart Philippines for more practical tips on how to save, insure, borrow, earn, and invest money within the local context.