Imagine you just checked your credit card mobile app and saw that your bank increased your credit limit to six figures. Are you happy? I bet you are. You may have considered withdrawing funds using the cash advance feature for fast cash withdrawals.

While a cash advance may seem like an easy gateway to borrowing money without the documentation, make sure you’re doing it right.

In this article, I will walk you through the credit card cash advance feature and unpack some moneysmart tips to ensure your credit card utilization isn’t max out.

Contents

- What is a credit card cash advance?

- How does a cash advance work and how to withdraw cash?

- What are the pros and cons of using cash advances?

- What are the alternatives to cash advances?

- What are the best practices for cash advance use?

What is a credit card cash advance?

A cash advance is essentially a way to borrow money quickly using your credit card, but it's different from regular purchases with the card. With a cash advance, you're borrowing cash against a portion of your credit card's limit. When you use your credit card to buy something, you're promising to pay the credit card issuer back later for the cost of that item.

How does a cash advance work and how to withdraw cash?

A cash advance is like a quick loan without credit investigation (CI) and documentation. It's handy in emergencies when you need cash right away.

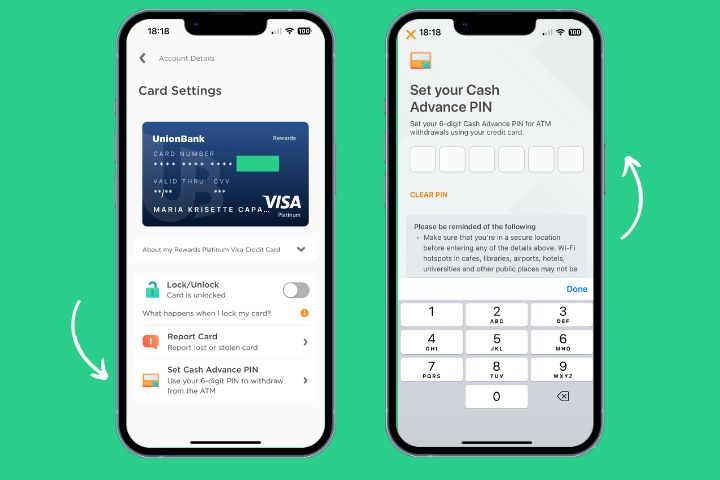

Like withdrawing money from your bank account using an ATM, you can get a cash advance with your credit card. You'll need a Personal Identification Number (PIN), which is a secret number to keep your transactions safe.

That PIN is on a piece of small paper that’s sealed and sent along in the credit card envelope mailed to your address. Usually, it’s a four-digit number that you can also reset via ATM. If you have a Unionbank-Citi mobile app, you can access and set that PIN yourself.

What are the pros and cons of using cash advances?

Let’s explore the pros and cons of using this credit card feature and if it’s even worth the risk.

Pros of cash advance

- Quick access to cash. One of the biggest advantages of a cash advance is the ability to get cash quickly, especially in emergencies. A cash advance can be a temporary lifesaver if you need immediate funds and can't wait for loan approvals.

- Convenience. Getting a cash advance is quite easy. You can withdraw money from an ATM using your credit card or get cash over the counter at a bank. There's no need to go through a lengthy application process, making it a convenient option when you're financially stretched before the payday.

- No need for a credit check. Since you're borrowing against your credit card's limit, there's no additional credit check required to access funds through a cash advance. This can be particularly helpful if you're concerned about your credit score.

Cons of using cash advance

- Additional fees. Aside from the monthly interest rates, cash advances also incur additional fees. In the Philippines, banks charge a fixed fee (usually around ₱200) for each cash advance transaction. This can add up quickly if you frequently rely on cash advances.

- Potential for bad credit score. Frequent use of cash advances can be seen as a sign of financial instability. Lenders and credit bureaus might view this behavior as risky, potentially affecting your credit score negatively should you decide to take out some loan in the future.

- Temptation to overuse. Because cash advances are easy to access, there's a risk of relying on them for regular cash needs. This can lead to a cycle of debt, especially if you cannot pay off the balance quickly.

- Lower cash advance limit. Your cash advance limit is usually just a fraction of your credit limit. This means you might be unable to withdraw as much cash as you need, even with a generous credit limit.

- No grace period for interest accrual. When you use the cash advance feature, interest starts accruing immediately after the cash is withdrawn. For every credit card cash withdrawal, the bank charges either a fixed amount or a percentage of the withdrawn amount, and interest starts accruing immediately.

What are the alternatives to cash advances?

I don’t have to sugarcoat the pros and cons, but the cash advance feature can negatively affect your credit card use and money management skills if you rely too heavily on it.

I’ve listed some cash advance alternatives you can consider if you need extra funds. Each one has its caveats, though.

1. Personal loans

Personal loans are a popular alternative to cash advances due to their lower interest rates and structured repayment plans. Interest rates are also lower than cash advance transactions. For example, HSBC Personal Loan offers a 0.65% monthly interest rate, and you can choose your payment terms, which are 6, 12, 24, or 36 months.

2. Borrowing from friends or family

Borrowing money from friends or family can be an interest-free alternative. This option usually doesn't involve formal paperwork or additional fees, making it a cost-effective solution for immediate financial needs.

It’s important to approach this option with clear communication and a repayment plan to avoid any potential strain on relationships that may end up with passive-aggressive innuendos publicly posted on your social media.

3. Short-term lending services

Short-term loans from online platforms or lending companies can also be an alternative to cash advances. These loans are designed for quick disbursement of funds, which can be beneficial in emergencies. However, you should carefully review the terms and interest rates, as they can vary widely and may be higher than other forms of borrowing.

What are the best practices for cash advance use?

When I was a new credit cardholder, I tried my best to build a positive credit score. As such, I used cash advances, especially when I was traveling overseas.

Withdrawing funds was a breeze, but I knew I had to stop it because I might end up in debt since I was still a money dumb at that time.

To ensure you’re still gaining good credit standing, here are some of the best practices for using cash advances.

- Emergency use only. Reserve cash advances for real emergencies. For instance, a cash advance can be a temporary solution if you suddenly need to pay for a medical expense and have no other immediate funding sources. You can also ask the hospital or clinic (especially if it’s a major one like St. Luke’s Hospital) if they accept credit cards. I’m betting they usually accept major credit cards, so you won’t have to make some cash advance withdrawals.

- Understand the costs. Be fully aware of the interest rates and fees. For example, HSBC Philippines charges a 3.04% monthly effective interest rate for cash advances. This means if you borrow ₱10,000, you'll incur around ₱304 in interest per month, plus a possible cash advance fee.

- Repayment plan. Before taking the advance, have a clear repayment strategy. If you borrow ₱5,000 for an urgent repair, plan your budget to repay it as soon as possible to minimize interest accumulation.

- Limit the amount. Only borrow what you absolutely need. If your car breaks down and the repair costs ₱7,500, don't be tempted to take out more than that amount just because you can. Now if your car is casa-maintained, dealers often accept major credit cards as well. Thus, it will more likely prevent you from using a cash advance.

- Avoid habitual use. Refrain from relying on cash advances as a regular financial tool. Continuously resorting to cash advances can lead to a cycle of debt that's hard to escape.

- Check alternatives. Explore other options before a cash advance. For instance, if you need funds for a business, consider a personal loan instead which might offer lower interest rates compared to a cash advance.

- Read the terms. Understand your credit card's terms regarding cash advances. Some cards may have different interest rates or fees for cash advances than regular purchases.

Final thoughts

It’s easy to see the appeal of cash advances—instant access to cash without the hassle of a credit check. While they can certainly be a lifesaver in times of financial emergency, it's important to understand the process and weigh the pros and cons before using this option.

Remember, great power comes with great responsibility, so use this financial tool wisely. Consider alternatives like personal loans or balance transfers with lower interest rates before taking out a cash advance.

If you choose this option, pay off the amount as soon as possible to avoid additional fees and interest charges.

Ultimately, think first before you use a cash advance option.

I hope that our comprehensive guide provides you with enough information to make educated decisions about your finances and avoid unnecessary financial stress in the future.

Have you tried cash advance? Let us know what you think in the comments section.

Do you find this article insightful? Share this article to anyone who needs to be moneysmart with their finances.