There are different ways to grow your hard-earned money. If you’re not satisfied with fixed deposit earnings or with investing in real estate, Bitcoin, or the stock market, then you may want to explore the PAG-IBIG MP2 Savings program.

Did you know that with MP2 Savings, you can earn up to a 7.00% dividend rate? This government-backed savings program is a low-risk type of investment that offers higher interest rates than commercial banks.

In this article, you’ll learn more about how it works and what you need to sign up for the program.

What is PAG-IBIG MP2 Savings?

The MP2 Savings Program is for PAG-IBIG’s active members who want to save while earning higher dividends. This is on top of their PAG-IBIG regular payments/savings.

It offers a 5-year maturity period, with the option to receive dividends annually or in five years.

Who is eligible for MP2 Savings?

Aside from active PAG-IBIG members, pensioners and retirees who were previously fund members can participate. However, they must have at least 24 monthly savings before retirement.

If you’re not a PAG-IBIG member yet, register and pay your monthly contributions to be an eligible member. Sign up via Virtual PAG-IBIG so you don’t need to go to the nearest PAG-IBIG branch.

But if you prefer to do it at the branch, simply fill out the MP2 Savings application form. Bring your valid IDs and ATM/passbook of your bank account where you want to receive your dividends.

How does PAG-IBIG MP2 Savings work?

The minimum remittance is P500. You may increase the amount, depending on how much you plan to invest for five years.

There’s no limit to how much you want to save. But if it’s more than P500,000, you are required to issue a personal or manager’s check.

You can start saving every month at P500 or do it lump sum of a higher amount.

PAG-IBIG grows your money through the interests charged from borrowers and through corporate bonds, time deposits, and government securities.

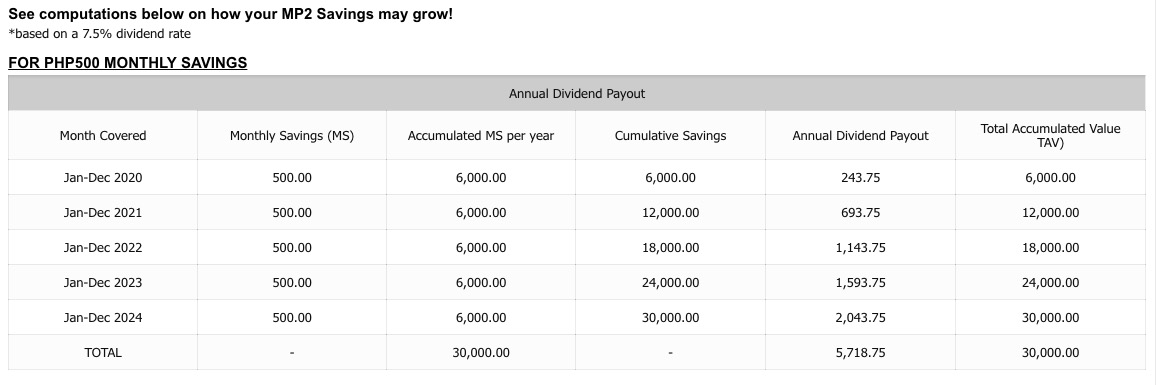

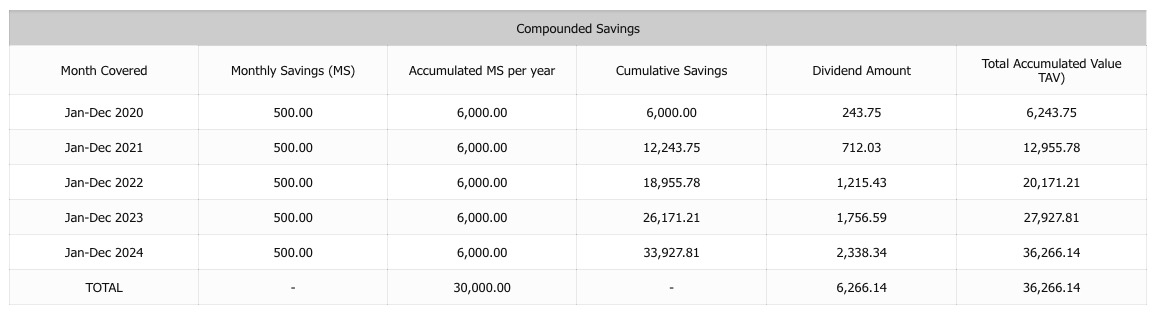

The computations from the PAG-IBIG official website are based on a 7.5% dividend rate, if you want to get an idea of how much dividends you will receive. These are not actual figures and only published for illustration purposes.

For annual dividend payout:

(Screenshot from MP2 Savings website)

If you choose the compounded savings:

(Screenshot from MP2 Savings website)

Based on the sample computations above, you will earn more with compounded savings than with annual dividend payouts.

Increasing your savings per month will also be beneficial for you. For example, you can start saving P500 for the first month, and then increase it to P1,000 the second month, and P1,500 the third month. You can choose how much you can put away, budget-permitting, of course.

There’s no penalty if you miss a remittance. If you remit P500 in your first month, make a P20,000 remittance in the second month, and then decide to just remit quarterly or annually after that, it’s totally up to you.

What’s more, this government-backed program offers tax-free dividend earnings at a rate higher than PAG-IBIG’s Regular Savings’ dividend rate. For your reference, the average

MP2 dividend rate from 2016 to 2018 was at 7.65%.

While earnings are guaranteed, keep in mind that the figures can change depending on PAG-IBIG’s financial performance.

PAG-IBIG MP2 Savings vs commercial bank time deposits

Let’s compare the interest rates per annum you earn and the initial deposit of MP2 Savings and different commercial banks’ 5-year time deposits.

Savings/Investment Program (5-Year Maturity) | Interest Rate Per Annum | Initial Amount Placement |

PAG-IBIG MP2 Savings Program | 7.00% or more | P500 |

BDO Premium Flexi Earner | Contact branch for updated rates | P10,000 |

China Bank Money Lift Plus | Floating rate | P50,000 |

EastWest Bank 5-Year Time Deposit | 1.625% | P10,000 |

Maybank ADDvantage 5-Year Time Deposit | Contact branch for updated rates | P50,000 |

PSBank Peso Prime Time Deposit (5-Year) | 2.2500% | P50,000 |

RCBC 5-Year + 1 Day Time Deposit | 1.875% 2.125% | P100,000 — P999,999P1 million |

MP2 Savings earns you higher interest rates. It’s also more flexible as you can start for as low as P500 and grow it every year.

But if you’re serious about diversifying your investments to meet your financial goals, get a time deposit and an MP2 Savings Account. While you’re deciding, you can read more about fixed deposits and interest rates.

Final Thoughts

MP2 Savings is a good option for people looking for a safe, low-risk investment. Not only does it offer a higher dividend interest rate, but it's also useful for your short-term and long-term financial goals.

The day you remit your first deposit is the start of the 5-year holding period. Should you decide to extend the account, you may do so upon maturity and re-apply for a new MP2 savings account.

You may also deposit your funds via a branch visit or use third-party platforms such as mobile banking and e-wallets. Just keep your transaction number for your record.

What do you think of the MP2 Savings Program? How can it help you achieve your financial goals for the next five years?