If you are an expat in the Philippines, you need a bank that will meet all of your banking needs.

You're in luck because there are quite a few global banks that have branches in key cities here, as well as local banks that provide world-class services. This certainly makes it easier for you to manage your finances and stay on top of your spending.

Opening a bank account is quite easy and only takes a few minutes, especially if you have complete documents required for account opening.

Read on to find out what you need to open a bank account and which banks are best for expats.

But first, here are some things to consider when choosing a local bank

In general, larger banks are the safer option compared to smaller rural banks. The latter usually offer limited services and may be difficult to access due to their small banking networks.

You can also do online banking any time and any day with major local and international banks, and as of 2026, most banks also let you open follow-on accounts fully in-app. See our rundown of digital banks in the Philippines for the fully online options.

Most banks are open from 9 am until 5 pm on weekdays. But there are also banks that have Saturday banking, which is a bonus for people who can't do their banking at the branch when they're at work.

Your deposits are insured up to ₱1,000,000 by the Philippine Deposit Insurance Corporation (PDIC), effective 15 March 2025.

For a deeper dive, read our explainer on the PDIC deposit insurance scheme and what it covers.

What you'll need to open an account

You need to make a personal visit to the bank of your choice with your documents and valid identification cards. The most common of which are the following:

- Valid passport

- ACR I-Card (Alien Certificate of Registration Identity Card) — usually required once your stay exceeds 59 days

- Local mobile number (required for OTPs and mobile banking enrollment, especially after SIM card registration took effect)

- Proof of address (lease contract or utility bill)

- TIN or PhilSys (National ID) number, where applicable

HSBC Foreign Currency Savings Account

With HSBC, you can enjoy world-class banking and safe banking transactions.

You can keep your savings in a secure bank and have a foreign currency deposit account in 11 different foreign currencies:

- (AUD) Australian Dollar

- (CAD) Canadian Dollar

- (EUR) Euro

- (HKD) Hong Kong Dollar

- (JPY) Japanese Yen

- (NZD) New Zealand Dollar

- (GBP) Pound Sterling

- (CNY) Renminbi

- (SGD) Singapore Dollar

- (CHF) Swiss Franc

- (USD) US Dollar

Other Features

With this account, you also get a contactless foreign currency debit card which you can use for debit transactions in the Philippines and abroad.

If you have an HSBC Premier account, you don't need to worry about a minimum maintaining balance on foreign currency savings. Learn more in our guide to HSBC Premier benefits and preferential rates.

You'll also receive text and in-app alerts whenever a transaction is made on your account, plus a consolidated monthly statement for all your HSBC accounts.

Get 24/7 access to your accounts with HSBC Online and Mobile Banking. No need to queue up at the bank to do bill payments or fund transfers.

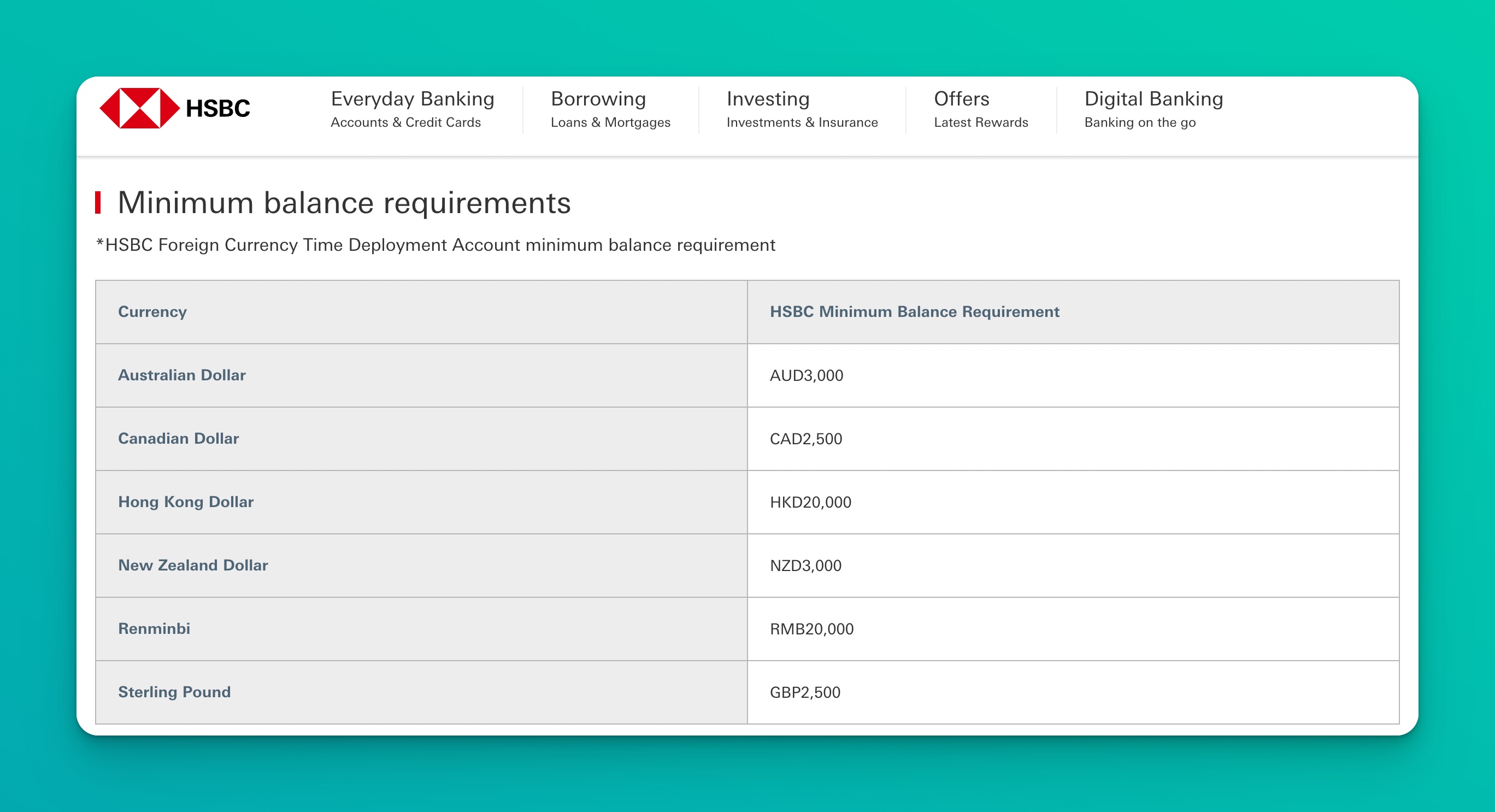

HSBC Foreign Currency Time Deposit Account

You have the option to lock up your funds for 1, 2, 3, 4, 6 months or 1 year. Foreign currencies available include USD, CHF, CNY, GBP, NZD, HKD, EUR, CAD, and AUD. For live rates, see the HSBC Foreign Currency Account page.

You can make over-the-counter withdrawals for foreign currency notes, but you need to make the request at least 3 working days in advance.

If you'd rather compare peso time deposits instead, check out our roundup of the best fixed deposit accounts in the Philippines.

How to apply for an HSBC Foreign Currency Savings or Time Deposit Account

HSBC Philippines now serves retail expats primarily through HSBC Premier. To qualify, you need a Total Relationship Balance of at least ₱3,000,000 (or its foreign currency equivalent) in deposits and investments, or a mortgage loan of at least ₱6,000,000.

Per the 2025–2026 HSBC PH Terms & Conditions, from 30 June 2025 a minimum TRB of ₱1,000,000 is required to maintain a Personal Banking account, with a Below Balance Fee if not met for two consecutive months.

The former HSBC Advance tier has been retired.

UnionBank Global Currency Account (replaces Citibank)

Citibank's Philippine consumer business was acquired by UnionBank in August 2022, so the Citi Global Wallet, Citigold, and Citibank Debit Mastercard products referenced in the 2020 version of this article are no longer available as Citi-branded offerings. Former Citi clients were migrated to UnionBank.

UnionBank now offers a multi-currency deposit experience through its foreign currency deposit accounts and mobile app, with USD, EUR, GBP, JPY, AUD, HKD, and SGD typically available. You can move between currencies in-app, link a debit Mastercard, and transact online without juggling separate accounts.

If you previously held a Citi credit card, our guide on UnionBank-Citi cash advances may be helpful. You can also compare options in our UnionBank Lazada Mastercard Rewards review and UnionBank Cashback Gold Mastercard review.

BPI Foreign Currency Savings

Enjoy convenience as you monitor your transactions and let your foreign currency savings grow with BPI.

Its Foreign Currency Savings Account is available for the following foreign currencies:

- USD

- JPY

- EUR

- GBP

- CHF

- AUD

- CAD

- CNY

- HKD

Most currencies require a 500-unit initial deposit and a 500-unit monthly Average Daily Balance.

You can choose from their Foreign Currency Passbook Savings account or the Express Dollar ATM Savings, and open an account at any BPI branch. BPI Family Savings Bank was merged into BPI in 2022, so there's no separate subsidiary to visit.

The Express Dollar Savings offers convenience and flexibility so that you can send and receive money via telegraphic transfers.

You can also receive dollar checks, cash, travelers checks or demand drafts. Existing BPI clients can open follow-on foreign currency accounts straight from the BPI mobile app.

For more on BPI's peso offerings, see our BPI Peso Savings Account review and BPI Preferred benefits and preferential rates.

Digital bank alternatives for everyday peso banking

If you only need a peso account for daily spending and don't require foreign currency features, the Philippine digital banks licensed by the BSP are worth a look.

Deposits are still PDIC-insured up to ₱1M.

- GoTyme Bank. Free Visa debit card printed on the spot at a mall kiosk; strong for expats without a local address history.

- Maya Bank. High-yield savings, integrated with the Maya e-wallet.

- Tonik Digital. Another alternative with competitive time deposit rates.

- UNO Digital Bank. Multi-"stash" savings with competitive time deposit yields.

- SeaBank and Komo Bank. Fully app-based onboarding for peso savings.

For a side-by-side comparison, see our roundup of digital banks in the Philippines that let you open a savings account online.

If you're new to the country and want a broader view of account types, our guide on the 7 types of bank accounts every Filipino should open is a good starting point.

Final thoughts

To help you decide, know which things are important to you when it comes to banking services.

- Are you looking for banks that have low fees or require a minimum balance? Do you put a premium on the accessibility of the bank and their ATMs?

- Or will you go for a bank with competitive interest rates, secure banking experience, or top-notch customer service?

If rate-hunting is your priority, check our guides on fixed deposits vs. high-interest savings accounts and savings accounts that actually earn.

The Philippines has more stringent banking requirements and regulations. Whichever bank you pick, make sure to read the terms and conditions before signing anything or handing over your hard-earned cash.

You may also want to review common online scams in the Philippines and how to spot a phishing email before enrolling in online banking.

Let us know in the comments which one worked best for you, and whether any of the newer digital banks have made it into your mix.