An amortization provides borrowers with a clear picture of how much they will pay during the entire repayment period of their loan. Read on to learn more about how your home loan’s amortization works.

What is amortization and how does it work?

Amortization is the process of spreading out a loan into several fixed payments over a period of time. Each month for a set number of years, you will be paying off the loan principal and interest at different amounts, but the total payment is still equal every period.

When it comes to housing loans, monthly payments remain the same, but there are parts of the loan that change as time passes.

A portion of your monthly amortization goes to the interest cost and settling the loan principal.

Interest costs, or what your bank gets paid for the loan, are the highest at the beginning of the loan, especially in long-term loans. A huge chunk of the monthly amortization goes to interest expense, and only a small portion of your payment goes to the loan balance.

In short, the early years of your loan don’t put in that much towards paying off your loan principal. But as you make more and more payments, you start to pay more for the loan principal and less on interest.

This is because the amount that you owe when you make your first few payments is bigger than the amount you owe when you make your subsequent payments. When compounded interest is applied to your initial loan balance, you get a higher interest payment compared to the balance of the last payment.

If you have an amortization, the goal is to pay it off as quickly as possible so that you can save money on interest.

What are the different types of amortizing loans?

Installment loans are amortized, and you pay the loan balance over a fixed period until the balance becomes zero.

Some of the most common amortizing loans are home loans, auto loans, and personal loans.

Home loans traditionally have a fixed rate mortgage, and the loan period could be anywhere from 5 years to 30 years.

Some homeowners keep the loan for the entire term, while others choose to refinance the loan or sell the home.

Auto loans are shorter amortizing loans, usually five years. It’s short for a reason. If you pay longer than five years, you end up spending more on interest, and the loan exceeds the resale value of your car.

Personal loans are often used for debt consolidation or small projects. Aside from banks, they are offered by credit unions and online lending companies as well. They usually have a 3-year payment period, fixed interest, and monthly payments.

How do you compute for your monthly amortization?

If you’ve always wondered how your bank computes your monthly amortization on your house, they use a factor rate to compute your monthly installment payments.

For home loans, you need the following information to compute for your monthly amortization:

- The property’s total contract price

- The amount that you will loan

- Equity or down payment (which is usually calculated by subtracting the loan amount from the property’s total contract price)

- Interest rate (this will depend on the bank, Pag-IBIG, or property developer if you will opt for in-house financing)

Most banks and financial institutions have an online housing loan calculator. It will give you an idea how much your monthly amortization will be based on the price of the property, your monthly income, or how much you want to borrow.

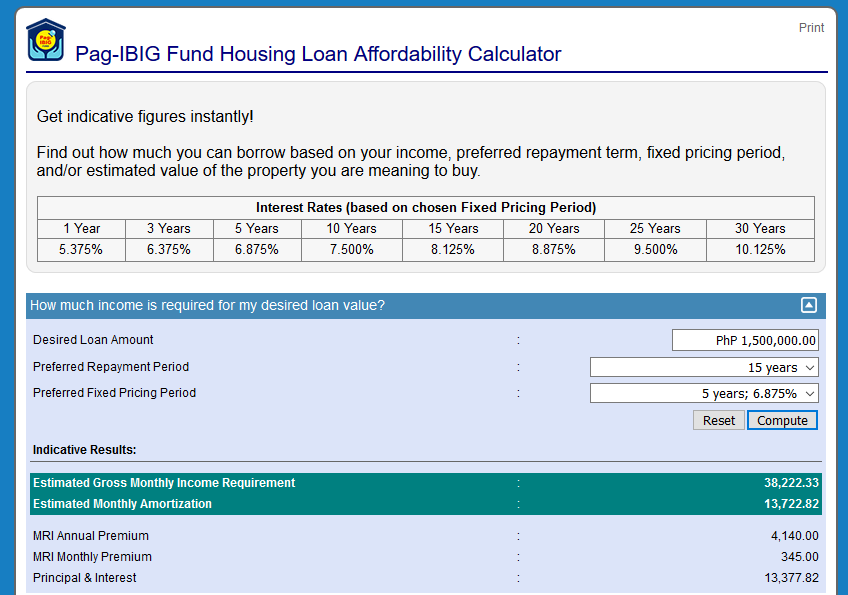

You can check out the Pag-IBIG Fund Housing Loan Affordability Calculator for a sample monthly amortization computation.

Screenshot taken from the Pag-IBIG official website.

These are indicative figures based on a desired loan value of 1,500,000 PHP for a repayment period of 15 years and fixing period of 5 years.

The estimated monthly amortization is 13,722. 82 PHP, and you should be earning approximately 38,200 PHP per month.

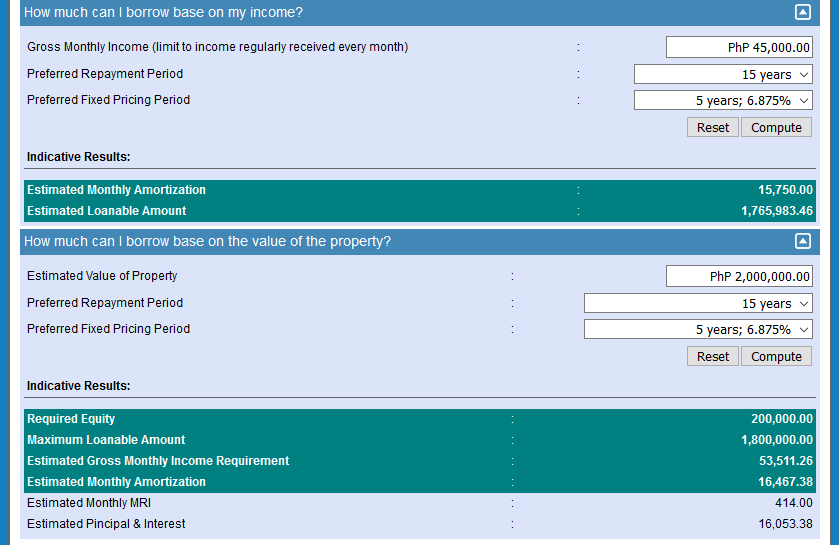

Screenshot taken from the Pag-IBIG official website.

This shows how much you can loan from Pag-IBIG by keying in your gross monthly income or the value of your desired property.

BPI, BDO, RCBC, and Metrobank also have home loan calculators on their website that you can try. Just key in the required information and you will get indicative figures for your home loan amortization.

What are the advantages and disadvantages of having an amortization?

You have the advantage of knowing how much you need to pay for your loan every time, including principal and interest. This, ultimately, gives you a more manageable repayment schedule.

With each payment that you make, you also build on your home’s equity.

The drawbacks to having an amortization schedule is, oftentimes, borrowers do not realize just how much they are actually paying in interest.

Monthly payments can also be quite high because you are paying for both principal and interest.

Conclusion

The financial side of amortizations can be quite confusing because of all the numbers involved. But if you look at your amortization table closely, it’s quite simple enough to understand.

Your amortization schedule will help you see how much your property costs with interest. The first few years, payments mostly go to paying off interest. But over time, a higher percentage goes to paying off the principal.

As the years pass, the principal that you owe on the property decreases and builds your home equity.

Some borrowers opt for the shortest repayment period, while others opt for the longest one possible. It really depends on the state of your finances and your long-term plan for the property.

But don’t forget that the sooner you pay off the loan, the less you pay in interest, resulting in financial savings and home equity that’s built more quickly.