Planning to purchase your ultimate dream home? Choosing the right housing loan could be a dilemma as financing is complicated and confusing to some. But it shouldn’t be if you research and compare interest rates and offers.

You could also take the in-house financing option, but the interest rates are higher. Another option is to apply for a home loan with a commercial bank. Unfortunately, if you lack documentation, you won’t get approved.

This article will help you weigh the pros and cons of a PAG-IBIG loan vs a bank loan based on your financial capacity. Let’s begin.

Contents

- What is Home Development Mutual Fund or PAG-IBIG Fund?

- What are the chances of getting approved for a PAG-IBIG home loan?

- Should you get a PAG-IBIG or bank loan?

- 5 Key differences between PAG-IBIG and bank loans

What is Home Development Mutual Fund (HDMF or PAG-IBIG Fund)?

PAG-IBIG is a government-owned and controlled corporation under the Housing and Urban Development Coordinating Council (HUDCC). The HUDCC aims to provide affordable homes and financing to Filipino families, whether locally employed, self-employed, or employed overseas.

PAG-IBIG memberships give you access to short- and long-term loans, calamity loans, and housing programs. Once you’re a member, you must pay the monthly membership contributions deposited to your PAG-IBIG Savings I.

If you’re an active member or contributor of PAG-IBIG for at least 24 months, you are eligible to secure a home loan. Although, it’s still subject to terms and conditions and requirements.

What are the chances of getting approved for a PAG-IBIG home loan?

PAG-IBIG will look into your loan application and assess the following factors:

- Member’s actual need

- Desired loan amount

- Loanable amount based on your capacity to pay

- Loan-to-Appraised Value ratio

The Loan-to-Appraised Value ratio determines how much money you can borrow for your home loan.

In simpler terms, LTV is the loan amount compared to the property value you want to buy. Let's say you plan to buy a house worth ₱1 million, and your loan application is also for ₱1 million. That means your LTV is 100%.

PAG-IBIG follows specific LTV ratios depending on the total loan amount, ranging from 50% to 90%. The higher the loan amount, the lower the LTV ratio allowed, ensuring that the borrower has sufficient equity in the property.

Remember that PAG-IBIG will only allow you to have an amortization of 25% to 30% of your monthly income.

The interest rates are effective January 1, 2022.

** Quoted rates are subject to change, visit PAG-IBIG news and events for updates

Interest Rate (per annum) | Fixed pricing period |

5.750% | 1 year |

6.375% | 3 years |

6.625% | 5 years |

7.375% | 10 years |

8.000% | 15 years |

8.625% | 20 years |

9.375% | 25 years |

10.000% | 30 years |

Should you get a PAG-IBIG or bank loan?

Many think PAG-IBIG is more lenient than banks regarding requirements and documentation. Unfortunately, this is not the case. Both of these financing institutions are equally stringent on eligibility and background checks.

Here are some of the practical truths about loaning via PAG-IBIG.

- Frankly, PAG-IBIG prioritizes low-cost and affordable housing loan applicants. However, if you are eligible, you can always visit the nearest branch for a quote and appraisal of the property.

- Property developers also have an internal agreement with financial institutions, so if they are not partnered with PAG-IBIG, it’s less likely you can secure a home loan.

- It’s rare to secure a home loan through PAG-IBIG if you plan to buy a mid-cost property worth ₱5 million or more. Bank financing is a better option.

- While you can loan up to ₱6 million, the money goes straight to the developer or seller. But developers prefer to deal with banks because they are more structured and have faster loan processing.

- Some developers have custom agreements with PAG-IBIG on the loanable amount applicants can avail. For instance, according to DMCI Properties, select RFO projects are only available for financing, and the maximum loanable amount is capped at ₱3 million only.

In short, not all properties can be financed via a PAG-IBIG loan. Although the interest rates are lower than the banks’ offer, only low-cost and affordable housing loans will likely be approved.

But there’s no harm in applying for a PAG-IBIG home loan if you plan to purchase the following:

- Fully residential house and lot or adjoining lots for up to 1,000 sqm only

- Residential house and lot, townhouse, or condo unit

- Construction or completion of a residential unit provided that the PAG-IBIG member owns the lot

The latest interest rates of PAG-IBIG are roughly the same and compete against bank rates. HSBC loan interest rate for a 1-year fixed pricing period is 6.150%.

PAG-IBIG Loan | Bank Loan | |

Interest Rate (per annum) | 3.000% - 10.000% | 6.150% - 9.500% |

Loan term | Up to 30 years | Up to 20 years |

Fixing period | 1 — 10 years | 1-10 years |

Repayment amounts | Relatively consistent because of the stable interest rate | Varies as fixed rates are valid for either 1,2,3, 5 or 10 years |

Loan Appraisal Value | 90-100% | 70-80% |

Maximum loan amount | Up to ₱6 million or 80% of the total accumulated value (TAV) | Varies, either in the amount or 70-80% of the appraised value of the property |

Miscellaneous fees for processing | ₱3,000 + | More or less ₱15,000 |

Processing period | Up to 15 business days or could take a few months | 5-7 business days or up to one month or more |

To summarize,

- PAG-IBIG and bank financing offer almost the same bracket in interest rates. But the former prioritizes minimum wagers and low-income earners and has a fixing period of up to 30 years.

- Banks may lower interest rates, but the fixed rate is only valid for 1, 2, 3, 5, or 10 years at best.

- You can borrow as much as ₱6 million from PAG-IBIG, but you need to meet the qualifications as an active member.

- Some property developers have a cap on the maximum loanable amount via PAG-IBIG financing and are only applicable to select RFOs.

- PAG-IBIG processing fees cost lower than bank loans, while the processing time is shorter on bank loans.

5 Key differences between PAG-IBIG and bank loans

Compare these key differences below to see which financing option is for you.

1. Loan purposes slightly differ

Securing a home loan will require you to disclose the purpose of the loan. Most commercial banks and also PAG-IBIG consider a new or re-purchase of a property like a townhouse or a condo unit, completion of home construction, and refinancing your property.

Meanwhile, PAG-IBIG allows home loan applicants to purchase a lot not exceeding 1,000 sqm. Commercial banks offer other services, such as home equity.

2. Interest rates and the maximum amount to borrow

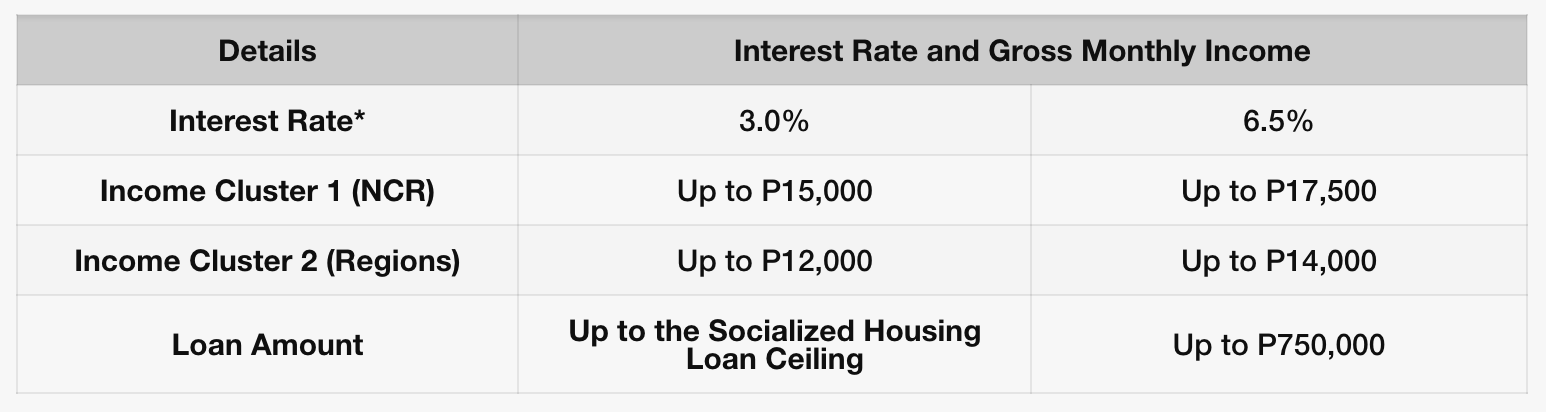

PAG-IBIG offers its members access to borrow up to ₱6 million, and those earning minimum wage can enjoy a lower annual interest rate per annum from 3% to 6.5% under the Affordable Housing Program.

[Image credit: Pag-ibig website]

However, to be eligible for this offer, the home loan applicant must have less than ₱15,000 as gross monthly income in the NCR region and P12,000 outside Metro Manila. They can avail of up to ₱750,000 of housing loans only.

Interest rates in commercial banks are almost the same as PAG-IBIG but have limited fixed rate terms that are good or valid as 1, 2, 3, 5, and 10 years. PAG-IBIG also has a fixing period of up to 10 years.

Acquiring an interest rate with a fixed term of 10 years means you’re spared from the market’s fluctuating rates (if your loan tenure is 15 years), usually higher than your original rate when you apply for the loan.

Once your fixed rate from the bank expires, you are at the mercy of the market’s prevailing interest rate. And that could be the same or higher, depending on the condition of the market and economy.

3. PAG-IBIG loans are better for repayment options

Repayment is repaying the lender the amount you borrowed, including the principal and interest rate, based on the contract. With PAG-IBIG loans, the repayment scheme is less complicated in computation, as the fixed rate is consistent for the loan tenure.

You can pay in a lump sum or at any time pay it in full, or you may wait until its maturity date. The maximum loan tenure is 30 years.

However, when it comes to home loans in commercial banks, the process and the computation are quite complicated and vary because the fixing period is shorter, and you also need to pay for the early repayment fee. Banks can provide you one to 10 years of the fixed rate at best.

If you have a stable income, a PAG-IBIG home loan is a good option if you don’t want to mess with the fluctuating rates from the banks once the fixing period ends.

4. Banks have stricter requirements and qualifications for borrowers

Compared to the list of requirements and qualifications between PAG-IBIG and commercial bank home loan applicants, the former is more lenient even to the new or first-time applicant.

PAG-IBIG members should have 24 months of contribution and no existing multi-purpose loans in arrears. Members can also pay 24 months of that contribution in a lump sum. And no history of PAG-IBIG loan had been canceled, foreclosed, or bought back.

On the other hand, if you apply for a bank home loan, you don’t have to be a member of PAG-IBIG, but your monthly family income must be more than ₱40,000 and proof of stable income.

Business owners and the self-employed must submit requirements to prove the profitability of their businesses or profession for at least two years, including financial statements and other supporting documents.

5. PAG-IBIG is more lenient on missed payments than banks

PAG-IBIG offers a more lenient grace period for missed payments compared to banks. If you miss a payment, you have more time to catch up before you get penalized.

In contrast, banks will declare foreclosure of properties if you miss payments. You’ll also hurt your credit rating and pay penalties and fees.

Such a lenient policy benefits those PAG-IBIG members experiencing financial difficulties or unexpected expenses.

Instead of struggling to catch up with payments or risking foreclosure, you can work out a payment plan with PAG-IBIG that suits your current situation, such as lump sum payments of the principal.

But don't rely too much on the grace period, as interest and penalty fees may still accumulate over time. Communicate with PAG-IBIG as soon as possible if you're having trouble with your payments, so they can provide you with the best solutions and avoid any potential legal consequences.

PAG-IBIG or Bank loan - what’s the verdict?

It’s hard to be subjective when it comes to these two types of loans. However, it boils down to your lifestyle, eligibility, and financial capability. Bank financing is better if you want more flexibility on terms, processing, property type, and interest rates.

If you can pay off your home loan early, PAG-IBIG is better since you can choose a fixed rate based on your loan tenure, and the repayment option is less complicated. But, the downside is, you’ll likely have slightly higher interest rates than most banks.

If you’re going to stay in your company for the long term, say 10-15 years, then it’s also an excellent way to take advantage of your employer’s contribution to the monthly membership at PAG-IBIG.

But a bank loan is a better option if you understand the housing market and know how to refinance your home after your fixing period. You get to enjoy lower rates, but you must be aware of the terms and conditions of repayments and the implications if you miss paying your monthly amortization.

The last thing you want is a bad credit history, right?

What’s your experience with PAG-IBIG and bank financing loan applications? Share them in the comments below.