A Facebook ad on your feed promises a zero downpayment option and a monthly amortization of ₱15,000 for a 2-bedroom condo unit in the city center. In a perfect world, you simply contact the agent, sign the papers, and pay your monthly due. Imagine your dream of buying a home is one call away.

Apparently, this doesn’t work in the life of a middle class — where inflation eats up your monthly income and interest rates remain high. Unless you have an exceedingly fat bank account like Sys, Villars, and Angs, you think before you leap like buying a condo in the Philippines. Keep these pointers in mind as a first-time condo buyer.

Contents

- Assess your current financial situation

- Set aside downpayment and closing fees

- Weigh in the pros and cons of your preferred location

- Window shop on property developers' projects

- Decide whether you buy pre-selling, RFO, or second-hand/rent-to-own

- Choose a reliable agent for your chosen property developer

- Prepare all documents required

- Read the fine print before signing the contract

1. Assess your current financial situation

First things first, assess your current financial situation. We know it’s not the most exciting task. But grab a pen and paper, or open a spreadsheet and list all your monthly income, expenses, and savings.

List all your current loans, credit card bills, and other debts. Seeing everything in black and white will give you a vivid picture of your financial health. Knowing your numbers will help you decide how much you can realistically afford.

You don’t want to end up “house-rich, cash-poor” and struggling to pay your mortgage — it’s either no or go.

2. Set aside downpayment and closing fees

Before getting lost in alluring promos and eye-catching property listings, focus on saving up money for the downpayment and closing fees. This money should be on top of your emergency funds.

Here’s what you need to know for each one:

- A downpayment is the amount of money you will need to pay upfront to qualify for a home loan. This can range from 10% to 50% of the property's value, depending on the lender’s requirements.

- Generally, 20% of the home value is a good starting point. This ensures that you have enough equity in the property and could qualify for a lower interest rate. Again, it depends on your financial situation.

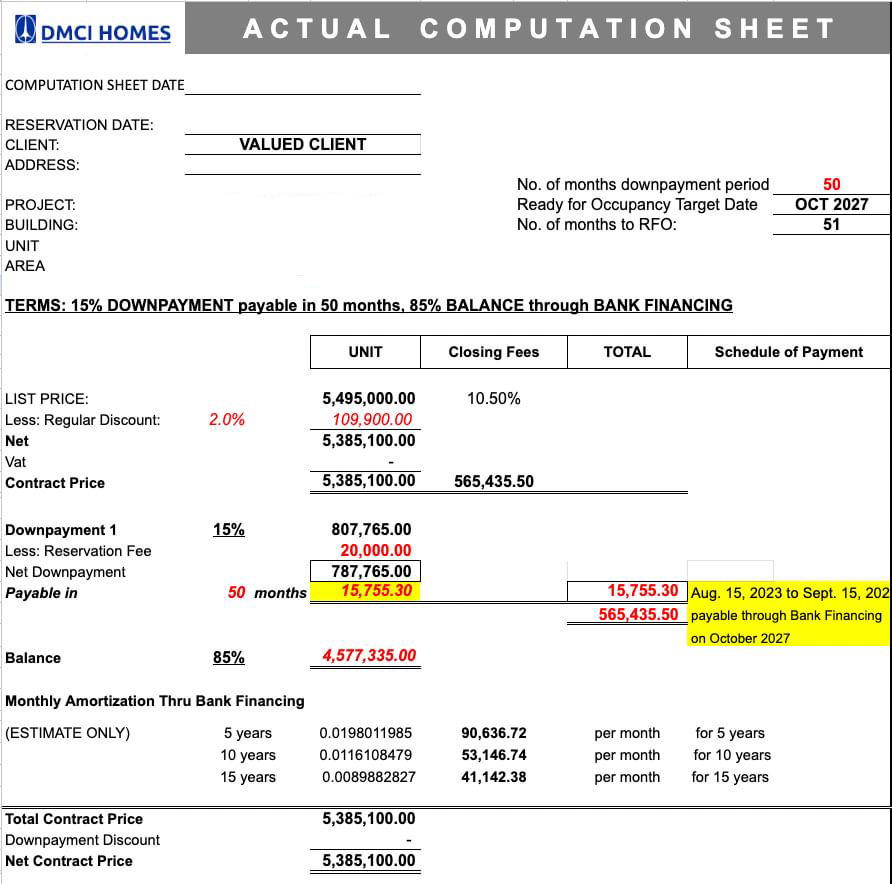

- Closing fees are an additional cost you need to account for. This includes taxes, title transfer fees, notarial fees, and other miscellaneous expenses. Failing to save up for these fees could surprise you before the turnover of your unit. Some developers charge about 10.5% of the net contract price, like DMCI.

Image: DMCI

One of the biggest mistakes of homebuyers is overlooking to account for closing fees. It’s easy to get caught up in the excitement of buying a home. However, the regret of not accounting for these fees will haunt you in the long run, as it can delay your closing date and finalization of your purchase.

3. Weigh in the pros and cons of your preferred location

The right location is substantially important for long-term comfort should you wish to reside in it and financial stability — as your passive income — if you rent it out.

When picking a condo, weigh the pros and cons of staying there, whether as a resident or a landlord.

Here are a few pointers to think about:

1. Is it near schools, hospitals, and shopping centers?

Consider the amenities and public transportation available in the area and whether they suit your lifestyle and routines. Determine the distance to and from your workplace or other major places you frequently need to visit.

2. Is the area near the site flood-free?

During the rainy season in the Philippines, flooding is a significant concern. To avoid inconvenience, choose a location with proper drainage or away from a creek or river. While high-rise condominiums are rarely affected, ensure the neighborhood has a reliable drainage system. Imagine commuting from work only to find the street leading to your condo impassable on a rainy day.

3. How safe is the neighborhood?

Check the area's safety and research the crime rates. High crime rates jeopardize your safety, mainly when walking in the neighborhood for essential errands. Avoid encountering skilled pickpockets outside your gated community.

4. Do you want high foot traffic or a laidback neighborhood?

The quality of your neighborhood can significantly impact your quality of life. Is the area noisy, or is it peaceful? Are there parks, community centers, and other places to socialize and make friends? Do you want to live near the train station despite the noise, or do you want the condo to be away from the main road for a laid-back ambiance?

When choosing a place to live, access to essential public services like hospitals, police stations, and fire stations is indispensable. So, list your negotiable (compromisable) and non-negotiable (fixed) factors for clarity and direction.

4. Window shop on property developers' projects

Window shopping, in this context, means looking at different options without committing to anything. By comparing property developers' projects, you get a sense of what's available in the market and how much you should shell out for your dream home.

Based on your assessments and checklist in the previous point, this will help you shortlist properties that match your expectations, lifestyle, and budget.

Research the reputation of the developer. Here are some questions to keep in mind.

- Are they known for delivering high-quality projects on time?

- Have there been any legal issues or complaints filed against them in the past?

- How does it handle condo maintenance and cleanliness?

Take note of the prices and payment terms. Consider the following:

- How much do you need to pay upfront?

- How much will the monthly amortization be?

- Are there any hidden fees or charges?

For your reference, here are the top property developers in the Philippines by net income.

5. Decide whether you buy pre-selling, RFO, or second-hand/rent-to-own

When buying a condo in the Philippines, you have three options. Let's briefly discuss each to give you an overview of what to expect.

What are pre-selling condos?

Pre-selling properties are still under construction. They are more affordable than RFO. There’s a bigger chance to choose a condo unit according to your preference, whether facing the city, sunrise, or sunset. But they have longer turnover periods, like two to five years — you won't be able to move in immediately.

What are RFOs or Ready for Occupancy units?

RFO properties, on the other hand, are already completed and ready for you to move in. They may be more expensive, but you can immediately move in and enjoy your new home. RFO properties are already complete, limiting design or layout changes.

What are second-hand and rent-to-own condos?

Second-hand/rent-to-own properties are previously lived in by owners or tenants and offer potential benefits. They are cheaper than pre-selling and RFO properties and provide room for negotiation on payment terms.

Additionally, you move in immediately through rent-to-own and lease-to-own schemes while securing ownership later.

However, be aware of potential risks and necessary home repairs.

6. Choose a reliable agent for your chosen property developer

Say you have cash, a preferred property developer, and the type of condo you want to buy. For RFO, rent-to-own, and second-hand properties, you may opt to transact directly with the owner. You’ll find these properties on Facebook marketplace, Carousell, Lamudi, and other real estate platforms. But the caveat is that you need to handle the legal papers, taxes, notarial requirements, to name a few.

For a brand-new condo unit, you need to find a real estate agent you can trust.

Real estate agents are licensed professionals who can help you find the property that suits your needs and preferences. They can also serve as a mediator between you and the property developer, being knowledgeable in market conditions, trends, and legal requirements.

Many agents will enthusiastically provide you with proposals, but not all provide quality service. Some focus solely on one-time transactions and may not support you afterward. Choose an agent who is committed to your long-term satisfaction, as they will be invested in your success in finding a home beyond their commission.

So, here are some tips to help you choose the right agent:

- Research thoroughly: Don't settle for the first agent that comes your way. Do adequate research on the real estate agents in your area, their track records, and customer reviews. Ask your friends or family for recommendations.

- Request for licenses and certifications: Investigate if the agent has the proper credentials and has a valid license issued by the Professional Regulation Commission (PRC).

- Check for experience: Look for an agent with at least five years of experience in the industry. This way, you can rest assured that the agent is knowledgeable in their profession.

- Look for specialization: Some agents specialize in specific areas of the real estate industry, such as residential properties, commercial properties, or foreclosures. If you have a specific property in mind, choose an agent specializing in that area.

- Compare commissions: Different agents may have varying commission rates, so compare and contrast their fees before settling with one.

Choose a trustworthy agent to guarantee a smooth property purchase. A reliable agent can make all the difference.

7. Prepare all documents required

The meaty and tedious part comes next — documentation. This is not an exhaustive list, but it will give you an idea of a list of what to prepare to process your condo purchase.

- Proof of identity: This could be any valid government ID with a photo. This is used to verify your identity during the transaction.

- Proof of income: This document is used to prove that you have a stable source of income to finance the purchase of the condo.

- Reservation agreement: It signifies your intent to purchase the condo. It usually comes with a reservation fee.

- Contract to sell: A legal agreement between the buyer and the seller that outlines the terms and conditions of the sale.

- Letter of Intent (LOI): It indicates your intention to purchase the property. Some sellers require this.

- Loan Guarantee Letter (if applicable): If you're taking out a loan to finance the purchase, this document from your bank or financial institution guarantees that they will cover the costs if you default.

- Deed of Absolute Sale: This document details the transfer of ownership of the property. It is filed with the Registry of Deeds once you've complied with the terms and conditions of the Contract to Sell.

- Certificate Title: This is issued by the Registry of Deeds in the city or municipality to certify an owner’s exclusive rights to a property. For a condo, a Condominium Certificate of Title is issued.

- Tax Declaration: This document is used to declare the property for tax purposes.

While the amount of paperwork may seem overwhelming for first-time buyers, it’s best to consult with a real estate agent or legal professional if there's any document or process you don't understand.

8. Read the fine print before signing the contract

Read the fine print before signing the contract, especially when buying a condo in the Philippines. Don't let the excitement blind you from reading important clauses in the contract.

Understand the terms and conditions before signing the contract. Ask questions if there's anything unclear or confusing.

Don't hesitate to seek advice from a legal professional or a trusted real estate agent.

Final thoughts

Purchasing a condo in the Philippines is a huge step, but it can be a very rewarding experience if done well.

Following these tips on buying a condo in the Philippines will help you go through this process confidently and get the best deal possible.

Having an experienced real estate agent on your side to guide you through your property options will also be incredibly helpful as you reach this huge milestone.

Are you ready to buy your first unit?