Are you tired of renting a place and dreaming of owning a home?

Whether it's a house or a condominium unit, owning a property is a big decision that requires careful planning.

Sure, you may have seen FOMO-induced advertisements of RFO (ready for occupancy) deals and pre-selling condos with low monthly payments, but have you considered the costs?

In 2022, the Philippines’ homeownership rate is 62.1%, which is relatively low compared to other Asian countries like Singapore, Vietnam, Japan, and Laos.

However, buying a home remains to be a significant milestone for anyone. But how do you know if you're financially ready for such a commitment?

In this article, we'll discuss the eight signs you should watch out for before moving towards homeownership — arm yourself with the knowledge to map out your budget and expenses.

Contents

- You have a stable income

- You can afford the monthly expenses, repair and maintenance, and association dues

- You have an outstanding credit score

- You can manage debt responsibly

- You can pay for the downpayment

- You have saved for the closing fees

- You researched and compared the interest rates and housing prices

- You are willing to sacrifice some comfort to become a homeowner

1. You have a stable income

What is a stable income? It means having a predictable, consistent source of money to cover monthly expenses, including a mortgage. This can come from regular employment, a business venture, or an investment that generates steady returns.

Consider multiple income streams to ensure your cash flow is consistent. They can help you maintain financial stability even during challenging times, such as a job loss or economic downturn, while paying your home mortgage.

Relying on a single source of income and committing to a long-term financial commitment is a recipe for financial disaster.

2. You can afford the monthly expenses, repair and maintenance, and association dues

Monthly payments are the regular expenses you must pay to keep your home. It includes utilities, water, electricity, and, most importantly, your mortgage.

Your mortgage is the primary expense you must pay monthly until you finish paying off the loan. Being able to afford these monthly payments means you have enough funds to allocate to your home expenses, even with your other essential needs.

Aside from monthly payments, you must consider home repairs and maintenance fees.

Generally, home repairs and maintenance fees can be divided into three categories: preventative, scheduled, and corrective.

- Preventative maintenance - Routine check-ups, cleaning, and replacing filters to prevent potential problems.

- Scheduled maintenance - Planned replacement of systems, such as an air conditioner or water heater, to keep your home in good condition.

- Corrective maintenance - Repairing damaged property, like fixing a roof or replacing a broken window.

For those who are planning to buy a condo unit, you are also required to pay for association dues.

Association dues are fees collected by the property management and used to maintain common areas like hallways, elevators, and amenities such as pools or gyms. Being aware of these additional fees will give you a complete picture of how much you will spend monthly, quarterly, and annually.

Some property developers also require you to pay parking and balcony/garden dues, on top of the condo dues. Make sure you include these fees as well in your budget.

3. You have an outstanding credit score

In the Philippines, a credit score is like a report card for your money habits. It's a three-digit number that shows how trustworthy you are when repaying loans.

Think of it as your financial superpower, rated from 300 to 850—with 850 being the ultimate high score. The higher your credit score, the more banks and lenders will trust you with their money. Of course, a good score means you'll get better loan deals and lower interest rates.

Having an excellent credit score means falling within the range of 700 to 850. It's like having a shiny gold star. This shows that you have an incredible credit history, and banks think you're a trustworthy borrower.

You may request your CIC credit report in person on the Credit Information Corporation website through their partner banks.

4. You can manage debt responsibly

Managing debt responsibly means handling financial obligations, like personal loans and credit card payments, without getting into some sticky financial mess. If you make those payments on time, don't go overboard on borrowing, and keep your credit score, you’re in tip-top shape.

So, how do you assess whether you’re good at managing your debts? Here’s a checklist for those who already have credit cards or existing loans:

- Timely payments - You pay credit card bills and monthly amortizations on or before the due date. You hate paying late fees.

- Ideal credit card utilization ratio - This is the percentage of your available credit that you are using. Ideally, you only use 30% of your total credit limit to show that you’re not overly reliant on credit cards.

- Pay more than the minimum - You pay more than the minimum amount of your credit card dues, and you even go beyond by paying the total amount due in full, and still, you are on top of other financial obligations.

Owning a home is awesome, but managing debt is the secret sauce. Here's why: Lenders want to see that you can handle money and pay off what you owe. They will check your debt-to-income ratio, credit score, and payment history.

5. You can pay for the down payment

In the Philippines, a down payment is like an upfront payment for a house. It's usually a percentage of the total price, ranging from 10% to 30%. If you can pay this in cash, it's one of the signs that you're ready to become a homeowner.

A higher downpayment can make a difference in your monthly mortgage payment and help you get a mortgage loan with better terms and lower interest rates.

Some property developers like RLC and DMCI have promos that offers flexible downpayment options for the pre-selling condo units to attract buyers.

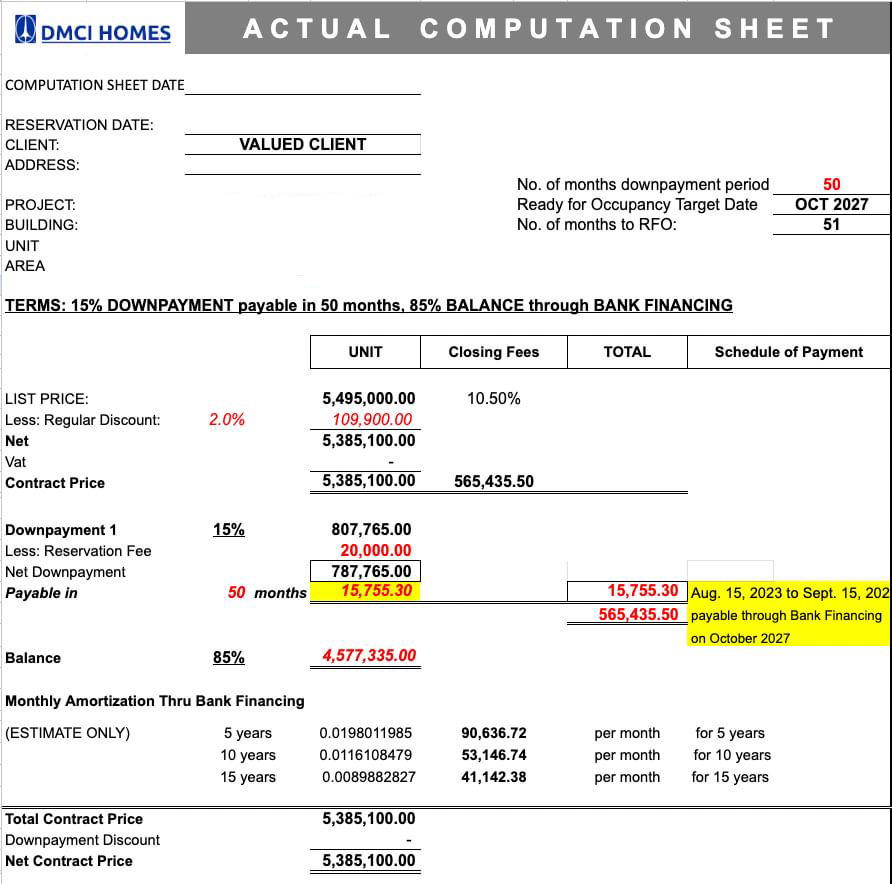

For example, a 15% net downpayment of a ₱5,495,000 condo unit less 2% discount — that’s ₱787,765, spread out up to 50 months, so you’ll start paying ₱15,755 per month. After 50 months, you either pay the 85% balance in cash or apply for in-house or bank financing.

Here’s an actual computation from a DMCI property specialist to give you an idea. The condominium is undisclosed. So, remember, these figures may vary depending on the day you requested a proposal from a property specialist.

Image credit: DMCI

Watch out for these promos, as you might think you’ll only pay less once you reserve a unit. However, the payment schemes will differ once you get the monthly amortization, including the interest rate with your preferred financing option and payment terms.

On top of that, you also need to consider your closing fees to be discussed in the next section.

6. You have saved for the closing fees

Closing fees in the Philippines are the costs to finalize a real estate purchase. These fees, added to the property price, are paid at the end of the process. If you have saved enough funds for these additional expenses, like taxes, registration fees, and more, you’re likely ready to buy a home. It's like budgeting for extra stuff when buying a house.

Here’s a list of closing fees in the Philippines you should know:

- Documentary Stamp Tax - When you transfer ownership of a property, you must pay a tax to the Bureau of Internal Revenue (BIR) to process the title transfer documents. This tax is 1.5% of the property's zone value or the contract price.

- Transfer Tax - The tax rate differs depending on the city. For properties outside Metro Manila, it's generally 0.50% of the property value. Properties within Metro Manila have a rate of 0.75%.

- Registration Fee - When you buy a property, you must pay a fee to the local Registry of Deeds. It's about 1% of the selling price. This fee is needed to get a new title with the buyer’s name.

- Notarial Fee - When you sell a property, you might have to pay a "notarizing fee" to make everything official. This fee usually amounts to around 1-2% of the selling price. It's like a little payment to ensure all the paperwork is in order.

- Loan fees (if applicable) - These include an appraisal fee (like getting a house value check-up), a handling fee (for the paperwork and stuff), mortgage redemption insurance (to protect the bank), and fire insurance (just in case the house needs some saving from fire).

7. You researched and compared the interest rates and housing prices

When you're looking to buy a home, spend time researching interest rates and housing prices.

Why?

Well, interest rates play a big role in determining how much you'll pay for your dream home.

When interest rates are low, buying a house becomes more affordable, which means more people are looking to buy. And you know what happens when there's high demand? Home prices start to rise.

On the flip side, when interest rates are high, the housing market slows down, which means you can snag a deal on a house.

Here are some practical steps in comparing interest rates and housing prices:

- Monitor interest rates and housing prices in the desired location by checking online resources, newspapers, and real estate listings.

- Consult with real estate agents or brokers who have expertise in the local market. Use online mortgage calculators to estimate monthly payments based on interest rates and housing prices.

- Compare various mortgage lenders' and banks' terms and conditions to find the best deal.

- Consider the potential impact of future interest rate changes on housing prices and mortgage costs.

- Analyze the historical trends of interest rates and housing prices in the desired location to make informed decisions.

So, how’s the housing market in the Philippines? It’s getting better lately, thanks to the country's strong economic growth.

If you're thinking of investing in real estate, it's essential to consider a few things. Rental yields in Metro Manila look pretty good, ranging between 3.55% to 7.40%, with an average of 5.40%.

But keep in mind that interest rates can greatly impact housing prices and mortgage costs. Even a small 1% increase in interest rate can make monthly mortgage payments go up a lot.

So, before you dip your toe in the market, do some homework. Drill down the interest rates, visit your preferred bank, ask for quotations, and always read the fine print.

8. You are willing to sacrifice some comfort to become a homeowner

The eighth sign you need to look out for is whether you are ready to sacrifice some comfort to become a homeowner — it means that you should be prepared to make some adjustments to your current lifestyle and perhaps forego some luxuries to prioritize your home investment.

This is important because owning a home comes with significant financial responsibilities, such as

- Paying for mortgage

- Property taxes

- Maintenance costs

Before jumping into homeownership, assess whether you have the stability and discipline to manage these expenses.

Moreover, owning a home is a long-term commitment, and you need to be ready for the challenges and sacrifices that come with it.

For instance, you may need to forego expensive vacations or unnecessary purchases to prioritize your mortgage payments and other household expenses. You must say goodbye to your “add to carts” on Shopee and Lazada, and even your weekly buffets and sumgeopsal treats.

Considering this factor and other signs we've discussed, you can confidently plan, act, and win financially in your journey toward homeownership.

Final thoughts

Owning a home marks a major milestone in life, and with the right financial plan, anyone can become a homeowner.

Congratulations to those who have achieved 8/8 on this checklist - you're ready for homeownership.

We understand that perhaps it isn't easy or realistic for everyone to meet all 8 signs at the same time. If you haven't achieved 5/8 or missed one of these points, there is still hope.

To get started, consider which areas need more improvement, such as saving more for your down payment or using credit responsibly to build your credit score. But above all, before buying a home, make sure you have established your emergency fund to keep you afloat during uncertain times.

Of course, counting the cost before buying can also go a long way in helping ensure that you are making the best financial decision possible.

Are you ready for your homeownership journey? Let us know in the comments below.