HSBC’s Home Loan allows you to purchase your dream home, construct it just the way you dreamed it, or refinance your existing mortgage so that you can lighten your financial load and enjoy more savings. Read on to learn more about it.

What can you get from HSBC Home Loan?

Flexible repayment options

You can choose the Straight-Line Scheme to help you forecast just how much your amortization will be. Your monthly payments will be fixed, allowing you to better manage your budget each month and prepare for other unexpected expenses.

If you prefer the Reducing Balance Scheme, you can save money on interest payments because the principal portion is paid off at the earlier stages of the loan.

Competitive interest review dates and repricing

You can choose from yearly or from 2, 3, or 5-year interest rate repricing options. Whichever you think is best for your finances.

Note that a shorter repricing period means lower interest rates, but they will be subject to change after the first year. They can go up or down, depending on the current market conditions.

If you choose a longer repricing period, you will pay higher interest rates but you will be able to secure your monthly amortization for several years.

Competitive loanable amounts

HSBC offers loan amounts between 700,000 PHP to as much as 50,000,000 PHP.

Fast loan processing and releasing

A dedicated Home Loan Specialist will keep you updated and give feedback regarding your application.

Once approved, home loan proceeds are also released in batches, depending on the stages of completion of your home construction.

What can you do with your HSBC Home Loan?

Your HSBC Home Loan proceeds can be used to purchase a property, to construct or renovate your property, to refinance, or to reimburse acquisition cost.

Loan proceeds can also be used for home equity.

How much can you borrow for your HSBC Home Loan?

The amount you can borrow depends on the loan amount that you apply for, the property value, and your capacity to pay.

HSBC has an online home loan calculator that allows you to get indicative figures of your loan.

You can calculate your monthly amortization by keying in your desired loan amount, loan term, and repricing period. Or calculate based on your monthly income or the value of your property.

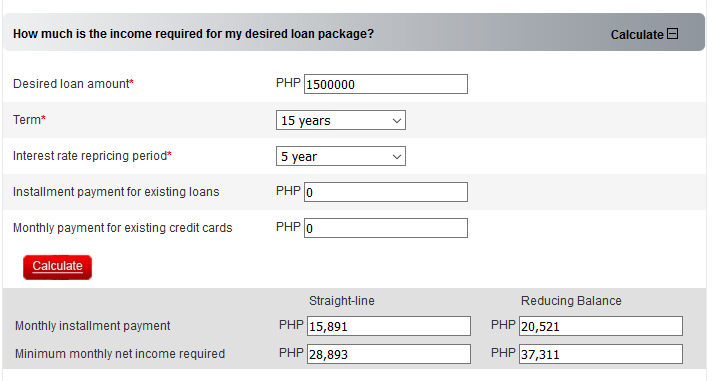

Here’s a sample computation of the monthly amortization for a loan amount of 1,500,000 PHP. It also shows how much your minimum monthly income should be.

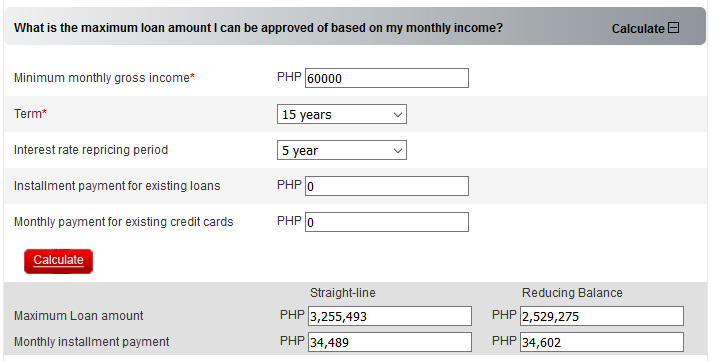

The next table shows the sample computation of a borrower with a 60,000 PHP monthly gross income, as well as their maximum loanable amount and monthly amortization.

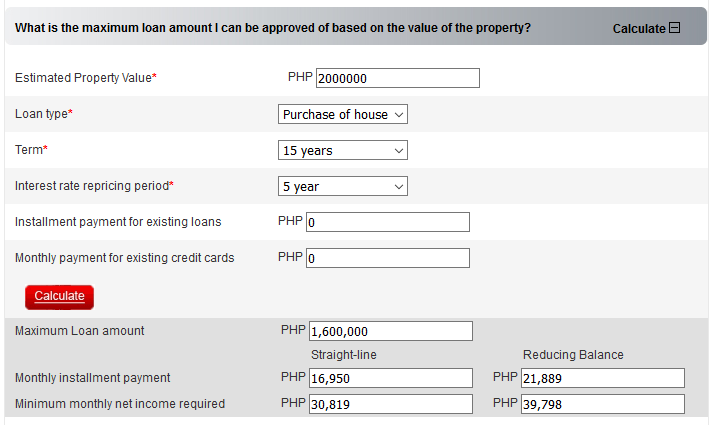

The third table shows how you can calculate for your maximum loanable amount and monthly amortization by keying in the estimated value of your property and the type of loan you are applying for.

Do note that these are all indicative prices only. Image screenshots are all from HSBC.

How long can you pay your HSBC Home Loan?

The minimum loan tenor is 1 year and the maximum is 20 years.

What are the eligibility requirements?

Existing HSBC Premier and HSBC Advance banking depositors can apply for the HSBC Home Loan and enjoy exclusive privileges.

To be an HSBC Premier client, you must have a Total Relationship Balance of 3,000,000 PHP or its foreign currency equivalent, be earning at least 300,000 PHP monthly, or have a home loan of at least 6,000,000 PHP for existing HSBC Advance customers.

To be an HSBC Advance client, you must have at least 100,000 PHP Total Relationship Balance or at least 2,000,000 PHP mortgage loan with HSBC.

Borrowers should be Filipino citizens who are at least 21 years old at the time of the loan application. The home loan should be repaid by the time the borrower turns 65 years old.

They should also be employed and have a permanent employee status.

For self-employed borrowers, the business should be in operation for at least 3 years.

A co-borrower may be required when the primary borrower does not meet the income requirements. If the co-borrower is related by consanguinity or affinity, up to 5 co-borrowers or guarantors are allowed.

What are the documentary requirements for the home loan application?

Refer to the table below for some of the documentary requirements that you need to furnish the bank when you submit your home loan application.

Locally Employed Borrowers | Self-Employed Borrowers |

|

|

What types of property will be accepted?

The following are acceptable types of property for the HSBC Home Loan:

- House and lot

- Condo unit

- Townhouse

- Vacant lot

- Accredited pre-sell residential properties of accredited developers

How do you apply for a home loan with HSBC?

You can fill out the online form to request a callback from the Home Loan Specialist Team. Key in your personal information, contact details, appointment preferences, and a few eligibility questions. Someone from the Home Loans department will then get in touch with you.

If you’d rather speak to someone on the phone, you can call the Home Loans department on the following telephone numbers:

Metro Manila: (02) 85800 or 976-8000

Provincial: 1-800-1-888-8555

Abroad: +6328580000

Conclusion

A home loan is a major financial commitment that will affect your finances for the next few years. That’s why it’s important to know the risks involved in taking out a home loan and have stability when it comes to your money flow.

HSBC’s Home Loan offers flexible features that can help you tailor-fit it to your needs as homeowners and mortgage holders.

What do you think of this home loan? Is it something you’d seriously consider when the time comes for you to purchase your dream home? Share your thoughts with us in the comments section!